Not De-Dollarise, but Re-Dollarise?

Is China planning to 'own' the Petro$ and by extension the Euro$ Market?

“In war, the way is to avoid what is strong and to strike at what is weak.”

SunTzu

The sale of a small amount of US$ debt last week by China may be nothing to worry about or it may be the start of something really big. We honestly don’t know yet.

Having wondered if the ‘October surprise’ might have been an announcement on a BRICS currency and a further push to de-dollarisation (nothing yet), perhaps what we now have is actually the opposite; a move to re-dollarisation.

The reserve currency status of the US$ is very strong, but the role of the Euro$ market is weaker. Trillions of US$ loans are effectively outside of the US and not regulated by the Fed. If China were to divert the Petro$ surpluses into China rather than US backed $ loans, it could then potentially ultimately ‘take over’ the supply and demand of offshore $ lending and by extension the soft power influence on the borrowing countries. Now that would be BIG….

A small bond transaction last week has seen some parts of the Twitter (X) sphere and financial bloggers getting rather excited. China just issued $2bn of dollar denominated debt, nothing special about that you might say, except:

It was issued in Saudi Arabia

It was 20x oversubscribed

It priced at 1-3bp above the equivalent US Treasury - making a mockery of the differential in sovereign debt ratings.

There are a number of ways to interpret this move. Firstly, it could be a test to see if China could access US Dollars in the event of its trade surplus drying up under Trump sanctions and its ongoing need for US Dollars to buy energy. As such it could simply be a demonstration of its likely resilience and thus a negotiating tactic with the new US administration.

Second it could be a different sort of negotiating tactic, more of a threat. China could be signaling to the new US administration that, unlike the traditional small countries issuing $ debt, it can compete directly with the US itself in accessing overseas markets for $s. Play nice or we will crowd you out of your own $ markets because while people may love the $, they hate the recent weaponisation of the US banking system.

Third, it may actually be showing its hand in a plan to effectively ‘take over’ the offshore Euro $ market. Instead of building an alternative market, perhaps, as Elon Musk did with Twitter, China thinks it’s just easier to reverse into the existing one? Don’t ask countries to give up using dollars, which they like, just to give up using them in the US banking system (which they don’t like). Steal the offshore $ banking market and you steal the soft power that goes with it.

China already has a lot of US$ it could lend, and earns around $1bn a day in exports, but the real key to this is the Petro$ market, the recycling of OPEC’s $ revenues from energy sales into US government debt which emerged 50 years ago in the wake of the Oil crisis. If OPEC countries switched to buy US$ bonds issued by China, then instead of funding the US current account deficit/capital account surplus, they would be adding to China’s capital account deficit, allowing China to lend dollars to the BRICS countries, crowding out US lending and perhaps even to pay off their existing $ loans.

In effect China has just demonstrated that, should it wish to, it has the ability to stage a takeover of the Petro $ market and thus put itself in the centre of recycling the US current account deficit

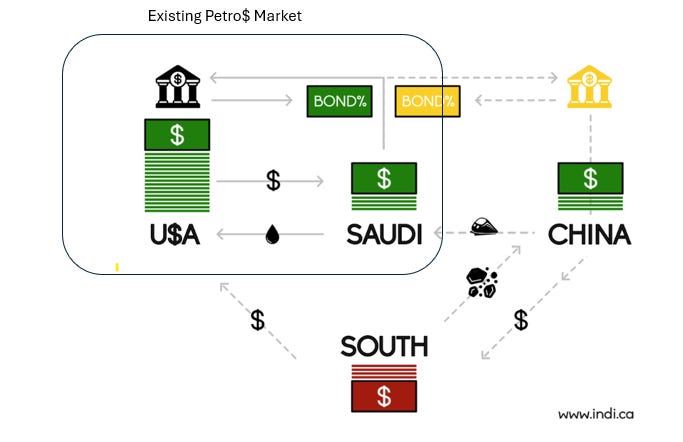

The above illustration (borrowed from here - with a bit of adaptation) highlights how the traditional Petro $ market in the top left of the diagram could be replaced with a new version, with China in the centre. Instead of Saudi selling oil for $ and recycling them back into US Treasuries - effectively giving the US control over how those $US are then spent - Saudi could effectively lend the money to China instead, allowing China rather than the US to decide what to do with them.

Instead of asking the Global South to accept Rmb loans, China could theoretically swap US originated (and controlled) US$ loans for Chinese ones

In particular that would mean China recycling those $US into the so called ‘Global South’ in return for resources (as it currently does with its own surplus $), but the twist would be that China could also effectively lend $US to the Global South for projects like the Belt and Road Initiative and theoretically also allow them to pay back existing $US debt to the US. The angle some are getting excited about is that some of the sovereign debt in US$ for the Global South could then be controlled by China - with all the geo-political implications that involves. Cherry picking the best quality, or strategically assisting in places like Pakistan and Myanmar?

It may just be that by weaponising the US$, the US authorities have just given up control of the Petro $ market and through it the offshore $ markets themselves…

One problem with this

The Eurodollar market at least had control of pricing via LIBOR That ended in September and SOFR is now the onshore benchmark

What benchmark thus would China use/create to effectively price this new offshore dollar pool ?