Supply Chain Cold War

Building Strategic Resilience. Market Thinking May 2026

The announcement at the end of April that the UAE (and others) need to access US dollar swap lines has potentially huge implications for the illiquid parts of US$ asset markets. If they try and redeem, price discovery could be brutal, but even if they don’t, where is the cornerstone funding going to come from to keep the show on the road? The only answer is governments, i.e. taxpayers.

The latest ceasefire from Donald Trump looked to be taking him through to the delayed meeting with Xi in Mid May, at which point he will try to look for a ‘Grand Bargain’, albeit with a weaker hand than he hoped. As of early May that appears to be fracturing, but the end game looks the same.

In effect, the Ceasefire in the Hot War leads to a Ceasefire in the Cold (Supply Chain) War. The US will ease pressure on Chinese energy imports, allowing it to build resilience, while the Chinese will ease pressure on the US imports of everything else, notably rare earths, but also things like base chemicals for pharmaceuticals.

Rebuilding strategic resilience - including cornerstone capital - will be a key driver of Cap-Ex globally and by extension profitability going forward. The ‘Post War/Cold War’ era is already well underway.

As usual, none of this should be considered investment advice. Please do your own research and contact your financial advisor.

Short Term Uncertainties - policy and liquidity

While the equity markets squeeze higher and oil reacts to every piece of news flow, the bond market is steadily voting for higher inflation - the only question now is whether we get an inflationary boom or an inflationary bust. In this, obviously the Straits of Hormuz are central, but we should also not lose sight of the issues around illiquid markets that the market was focussing on ‘pre-war’. These have not gone away and what has been largely overlooked so far in our view is that the Middle East were the cornerstone of almost every Alternative Investment in recent years.

The more significant impact from the UAE news this month may be that it is asset rich and cash poor and nobody wants it to try and sell assets. After all, they were the main buyer, so who would they sell to?

At the end of April, the UAE made a couple of significant announcements which we discussed in more detail in a separate note (see swapping out of OPEC). First, they - apparently along with others - asked for access to US dollar swap lines from the US Treasury, implying they are facing a liquidity squeeze and second, they announced they are leaving OPEC with immediate effect.

Both have increased uncertainty and the initial reaction of spot oil markets, to rise on higher risk and uncertainty, was contradicted by the long end of the curve, which sold off on the prospects of higher supply. However, in our view the market has yet to digest fully the implications of the swap lines. Our take is that the US is offering (limited) Treasury swap lines as a signal to the Fed that they may need to offer unlimited swap lines because the last thing the US wants is for the asset rich but cash poor Middle East to start trying to sell illiquid assets.

The last thing that ‘low risk’ assets want is a mark to market 30-40% lower for a distressed seller. This would trigger a ‘margin call’ on the pyramid of leverage sat on top of that cornerstone.

This is not about liquid assets like Treasuries - the US can simply print money and buy those and indeed, not paying out hundreds of billions in coupons to go outside the country would be seen as a positive. Rather, they are concerned, rightly, that Middle East investors would try and redeem some of the illiquid assets they have been sold in recent years. The myth of low risk as measured by low volatility risks being exposed by a forced mark to market and it won’t be pretty.

But even if they can hold off selling, a more existential question appears, who is going to be the cornerstone buyer for all the new investments required in the US and, even more important (for them) who is going to buy the products designed to create liquidity for the US Financial intermediaries? To keep the whole show on the road, VCs, PEs and PCs need IPOs or trade buyers and with Software as a Service Companies no longer buying up startups, the MAG 7 spending on physical AI infrastructure and the IPO markets still largely closed, the Middle East Sovereign Wealth Funds had been key players. Until now.

Doanld Trump is not alone in looking for an exit strategy from the war- the whole world of Private Capital is and the war has just made it harder

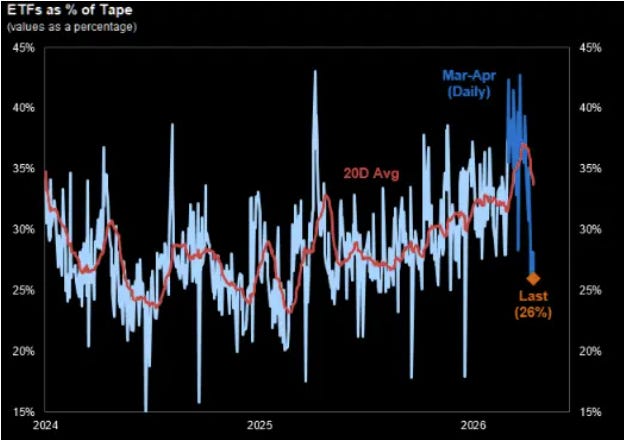

The Growing importance of ETF flows

In liquid markets, liquidity is also important. The chart from Goldmans shows the dominance of ETFs as a % of the tape dropping sharply over the last month, from over 40% to around 26%. Our interpretation would be two fold; first that the macro traders use ETFs as a ‘'fast hedge’ and second that there has been a growing shift to US Retail investing via ETFs and that, as per our comment last month, US retail stood aside during March and April (but came back at the end).

We believe that the rotation in early 2026 into the diversification trades that we prefer was partly driven by US retail buying ETFs in areas like Emerging markets, Mining and Nuclear, all of which then saw considerable ‘profit taking’ followed by first, short selling at the stock level and then subsequently by sharp squeezes higher during April.

A classic example would be Nuclear, an obvious beneficiary of the long term shift from fossil fuels, which nevertheless sold off heavily in March, before gaining most of it back in April - as shown in the chart below.

As previously noted, US Retail was largely absent during April as the CTAs and other traders first went aggressively short, then flipped to long as the squeeze kicked in. As US retail returned, they resumed buying many of the themes they just took profit in - exaggerating the squeeze.

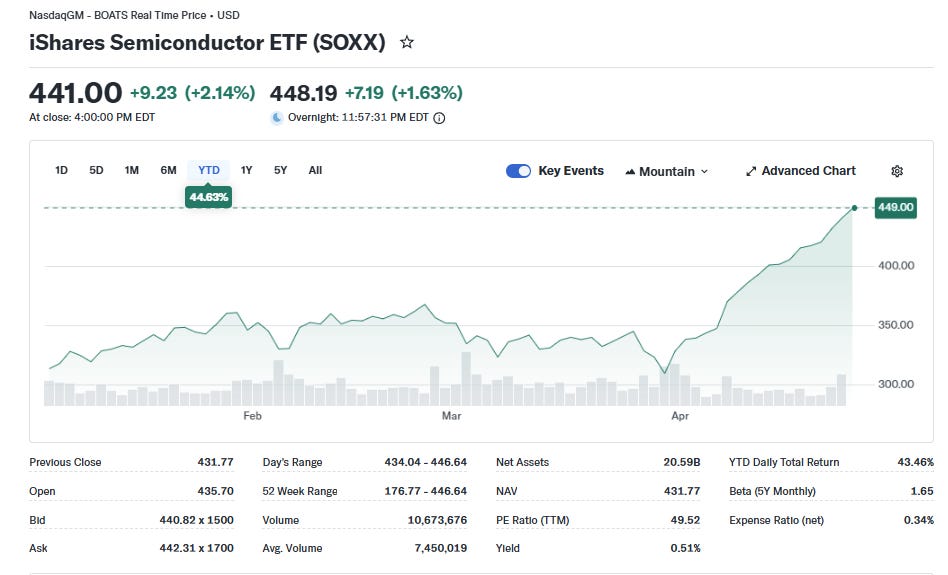

Elsewhere, ‘the only game in town’ for traders appears to be the Semi Conductors index (SOX), as part of the 'Hardware not Software’ trade in AI.

The biggest driver of this is, of course, Micron, which is why the South Korean market - dominated by the other two main ‘hardware plays’, SG Hynix and Samsung - is also up almost 30% from the end of March and over 50% year to date. This is also a reason why another ETF that we like, EMXC (Emerging Markets ex China), has also had a great month in April, it is basically dominated by Asia tech hardware like SG Hynix and Samsung, but also TSMC.

Macro traders had sold ‘emerging markets’ on a strong dollar and an imported energy thesis only for bottom-up investors to play the AI infrastructure trade more globally. The US and other retail investors basically re-appeared and started buying up the narrative names, which had read across via stocks to other ETFs such that chasing Global Semis or Korea had the effect of pushing up the EMXC ETF.

Medium Term Risks - the supply chain cold war.

To talk of the US stock market hitting all-time highs is basically to say that it has recovered from the war sell-off and is up around 5% year to date. Once again, the ‘do nothing’ strategy looks like it has paid off. At the index level at least. The split between Software and Hardware has been spectacular of course, but, as an example, the VanEck Rare Earth and Strategic Metals ETF, REMX, was up 17% in April month and 36% year to date. Global mining (GDIG) and Copper miners (COPP) are up around 16% year to date, while as discussed earlier, Nuclear has regained most of its profit taking from the start of the war to be up a similar year to date.

This is showing some significant opportunity for generating that elusive thing, ‘alpha’ and there are echoes of the early 2000s after the TMT bubble burst, when most strategies that were equal weight outperformed anything (like an index) that was market cap weighted.

The post war likely glut in oil production is currently priced into the long end of the oil curve - exaggerated by the prospect of OPEC collapsing and with all governments looking for supply chain resilience the strategic metals and minerals part of the materials sector continues to attract a lot of attention.

We should not forget the other pre-war obsession - Greenland and the Arctic

The medium term is thus essentially about a continuation of the pre war trends focussing on issues like the Arctic and Greenland, as well as the incorporation of the resources of Latin and South America into US supply chains. This is a return of Dirigiste Government as the US government, ironically, learns two lessons from China, first that industrial policy needs to be seen as a form of venture capitalism (in 2019 there were 500 EV companies in China, now there are 125) as opposed to a gravy train for Crony Capitalists and the CEO class. Second, they need to secure vertical integration of their supply chains rather than outsource in order to maximise short term profits.

Europe’s best hope is that technology and outside forces save them from themselves

Meanwhile, the ongoing economic self-harm in the UK and Europe - with seemingly the entire political class focussed on a combination of economically destructive Climate Change Policies and maintaining the war in Ukraine - is leading investors to, rightly in our view, vote with their feet.

They may, however, be saved by external forces, Battery Technology for example is evolving fast with Sodium and Aluminium rather than Lithium and copper allowing for lower costs and removing bottlenecks and offering the opportunity for scale storage, the only way renewables make economic sense.

Many small players, but also, particularly, the big players, CATL and BYD are now working on Grid level Sodium storage solutions which would transform renewables to reliables and offer the opportunity for Europe to actually deliver on its promises of cheap renewable energy and energy security.

Equally, for all the rhetoric, the end game for the Ukraine conflict lies not with the EU but with Russia and the US. As with the Iranian situation, there may be escalation to achieve de-escalation, but ultimately the economies of the EU may be bailed out despite the best efforts of their ‘leaders’. In the meantime, international capital is not sharing the vision of a ‘regulatory superpower’.

Long Term Trends - shifting alliances and building resilience

While the Iran War is not (yet) over, we continue to see the building of the alliances for the Post War era. Team Trump continues to make noises about leaving NATO, which now appears to be coalescing around a re-arming and German led NATO 3.0 (nothing alarming there then!) The biggest losers of both the Ukraine and Iran wars have been Europe, and the biggest winners so far have been China and Russia.

As discussed, with the UAE leaving OPEC, it will be trying to pump more oil than its current cap at 3m bpd, likely as much as 5m a day. In the short term this is obviously not going to happen due to the war - and the Iranians have just bombed UAE’s outlet on the Gulf of Oman that was allowing it to bypass the Straits of Hormuz to guarantee that. Longer term however, the fracturing of OPEC means lower oil prices.

This is only going to be compounded by the ongoing developments in energy tech, meaning, strange as it may seem right now, we are likely to move to an energy abundant world, which is going to be very important for the most energy constrained in the emerging world, particularly we think places like Africa.

However, for every 10 winners there is a loser and lower oil prices are not good for Saudi Arabia in particular, which needs $90-$120 oil to balance its budget and this will leave no room for investment in trophy assets like Football clubs and illiquid US alternative investments. Similarly, the UAE, which can survive on lower oil prices, is also very dependent on tourism and other financial services, for whom the post war landscape is very uncertain. Again, as some of the biggest buyers of US illiquid assets and weapons, their liquidity constraints will threaten two of the US’s largest export sectors.

Team Trump had previously been pushing for Petro Dollars to be recycled into ‘real assets’, with trillions promised for AI data centres and other investments to MAGA. Those are obviously very much under question now, with fewer petro dollars to go around, it spreads the threat from the Jenga tower in the heading picture into the whole AI infrastructure space. The only alternative is government spending, which is not going to make the bond markets happy.

Finally..can the world be saved by Lego?

China and Russia have almost zero propaganda impact on the west, but Iran is proving a very different opponent. They produced a series of powerful AI ‘Lego’ videos that were then deleted from YouTube but they continue to surface on X and elsewhere (like substack). This one is, as the commentator says, pretty Wow.