The Liquidity Sponge

The AI machine needs passive investors to get them liquidity

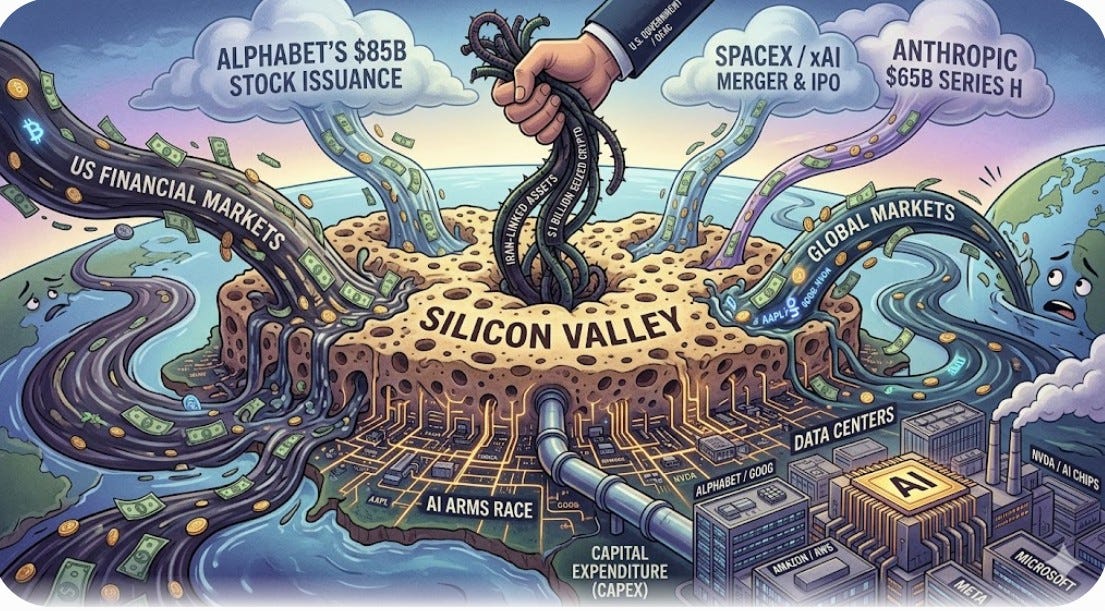

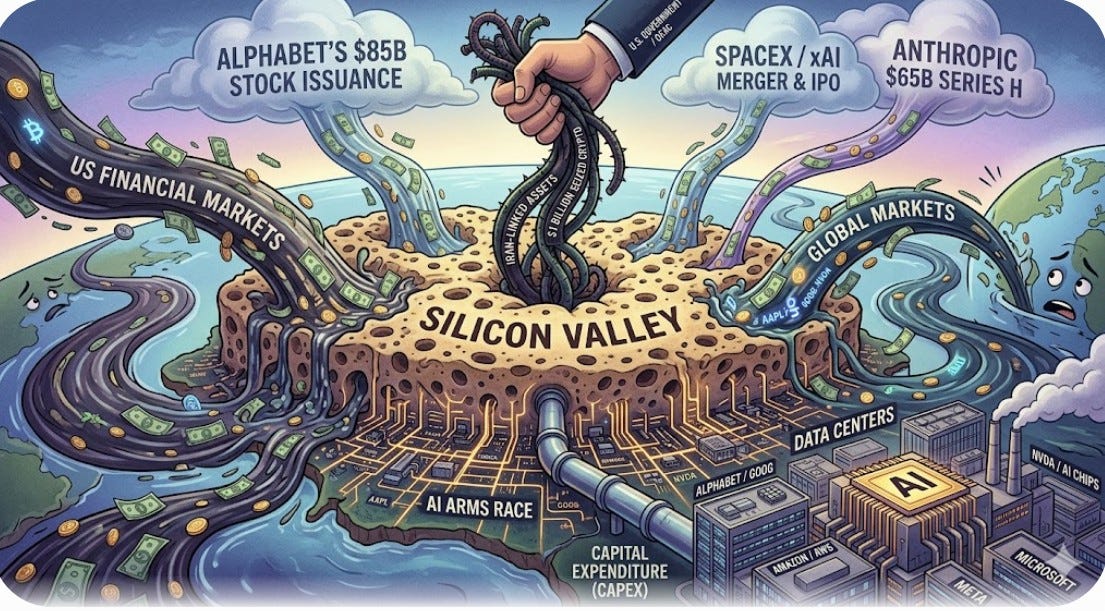

The narrative is flipping from bid to offer. After a decade of hundreds of billions in buybacks, Google just issued $80bnn to fund its part of the AI Cap Ex boom

The rest of the Mag 7 are also having to flip the narrative from software to hardware and balance sheet to cashflow. Meta is also said to be looking to raise ‘significant amounts’.

Michael Saylor of Strategy just sold some Bitcoin to pay a dividend and the price is crashing.

Space X, Open AI and Anthropic are looking to raise a further $200bn+ and are relying on the passive investors to do it for them.

A lot of people (not just the Bankers looking to raise $1bn in fees) need the markets to hold up so that they can extract liquidity, but holding equity markets up, like holding oil markets down, is not a long term strategy.

What Gets Measured, gets managed.

The quote (attributed to Peter Drucker) that “"If you can’t measure it, you can’t manage it”, is sometimes represented as “what gets measured gets managed”, shifting the focus from a need for accountability to an unnecessary focus on things that can be quantified. As it is sometimes said in this context, “Not everything that matters can be measured and not everything that we can measure matters.”

Here we would point to Government’s obsession with GDP numbers or the bond market’s obsession with employment data that gets revised away almost immediately, or, more pertinently for fund managers, the focus almost exclusively on volatility and correlation as measures of risk for long term investors. They can be measured, so they can be managed - and duly are managed regardless of whether they are the right things to measure.

However, there is a third interpretation of this - if something can be measured and is deemed to matter, then there is an incentive to manage it. Which brings us to markets right now.

Oil Prices and Stock Markets can be measured - so they matter. Ergo, are they being managed?

Much has been made of President Trump’s 3,700 trades in US Tech Equities in the first quarter alone and there are widespread concerns that insiders appeared to trade in equities and Oil around the time of significant posts on Truth Social. The oil trades should definitely be investigated and so indeed should the President’s - although the sheer volume suggests that he has probably got an AI driven high frequency quant algo working for him. However, our focus is on the ‘management’ of the measured indices to support a narrative.

Right now, the US stock market has become a measure in its own right, Team Trump point to the stock market at all times highs, suggesting that all is right in the world and that ‘the market agrees’. Same with the oil price (as measured on the screen). But is it? And does it?

It certainly appears that the US stock market is indulging in some magical thinking at the moment. The longer the war with Iran goes on, the more pressure there is on the global economy, and the more long-term damage is done. To the extent that stocks ultimately reflect earnings per share and to the extent that these ultimately depend on a robust Global economy, the powerful rally in April, extending into May certainly looks counter-intuitive.

The daily swings in the news cycle about on/off ceasefires do not obscure the issues over an inflation pulse already in the system and the bond market is saying that it doesn’t know if it is an inflationary boom or an inflationary bust. But the stock market only seems to care about AI.

Team Trump need the Oil Price low and Stock Market Confidence high for political reasons. Wall Street and Silicon Valley need the stock market high in order to extract huge amounts of liquidity for AI

Which brings us to what is being measured - and what is being managed. This is a third interpretation of the quote, the management/manipulation of the thing being measured - in this case the passive index funds and the market cap weighted benchmarks.

Everyone needs the AI story to work

With ‘everyone’ looking forward to the exciting - or should that be exiting? - IPOs from Space X, Open AI and Anthropic, looking to raise in the region of a combined $230bn, Silicon Valley and Wall Street need the Market Cap weighted indices like the S&P500 and NASDAQ to be confident and at all-time highs, because they need the passive index funds to soak up the issuance - and enable the insiders to get out.

Distressed sellers and forced buyers cause the most dramatic moves in prices

To this end, what can be measured (Indices) are being managed to ensure this happens. Listing rules and free float rules have just been changed such that the Indian rope trick of inflating valuations from VC through PE and PC can continue and Elon Musk - first off the rank - can sell less than 10% of Space X on a valuation that would rank it at almost 3% of the index, creating a completely false market as the passive funds become forced buyers.

This will probably work, but it’s not without risk. Meta popping up again will probably trigger a few memories of how its IPO went; a 50 per cent fall. The fact that it has done so well since is a not a reason to buy, rather the opposite. If you are a long term investor, why be part of the price discovery process? Why not wait a bit? (At this point we should probably say that none of this should be considered investment advice, please do your own research and speak to your licensed representative)

Meanwhile, the steady realisation that, having enriched themselves massively with share buybacks over the years, the tech-lords are going to be issuing stock, not buying it, is starting to sink in.

Short Term Uncertainties

As we head into the summer season, markets have a distinctly ‘toppy’ feeling to them and many are starting to wonder about the concept of ‘sell in May’ coming a week or so late. Certainly the wobble in NASDAQ on Friday will have triggered a few stop loss signals as well as a few more qualitative thoughts about ‘banking profits’.

This should make for some nerves in places like Goldman Sachs and Morgan Stanley as they need the hype and excitement to extend into the Season of Summer Sales as they plan to generously allow Retail Investors to participate in the exciting upcoming IPOs of Space X, Open AI and Anthropic, or perhaps more correctly to allow a whole host of industry insiders to get out of their existing positions while the banks take hundreds of millions in fees (around $500m for Space X and $600-900m for Open AI).

Wall Street is looking at $1bn+ in fees over the summer. Just need those passive investors in 401ks to participate

Elon Musk has started the ball rolling with his Space X issuance - a mind boggling $1.75trn valuation is based on a ‘modest’ actual raise of $75-80bn. As with everything Musk, his S-1 prospectus is full of symbolism - he is issuing 555,555,555 new shares for instance and 5% of those will be set aside for employees who can sell with no lock up. Musk, along with other early-stage investors, including Google are under a 180 day lock up.

In fact, Google went first

Next up is Open AI, looking to raise a $100bn similar amount and straight after that Anthropic, looking for $50bn plus. This, note, is straight after raising $122bn and $65bn respectively from the private markets. All of this is going into a massive Cap-Ex build out for AI. It is worth noting however that Alphabet (Google) just raised $80bn for the same purposes. And that has shocked investors, after years of buybacks, it is suddenly issuing.

Bitcoin is also facing a flip from a constant bid to a sudden offer

Meanwhile, after a brief rally at the beginning of the year and a post war bounce, Bitcoin is heading back towards 60,000. As we discussed before Christmas in our December Market Thinking (see Untethered from Reality ), the rise of Stable Coins like Tether has undermined a big part of the use case for Bitcoin beyond that of moving ‘hidden’ money, something which admittedly saw a sharp increase in demand in both Venezuela and the Middle East earlier this year. But even this is under threat; the US government has recently seized a significant amount of Bitcoin associated with scams in South East Asia (and allegedly linked to Iran) and clearly prefers a world of traceable and indeed programmable crypto.

The fact that the US Government now holds in excess of $24bn of Bitcoin is something the market is trying to get its head around - tightness of markets, rather like the squeeze being attempted by Space X et al, has been a key prop for the price of Bitcoin. A steady seller is hardly welcome.

This is why the market is now so worried about Strategy and Michael Saylor, who just sold a small amount of bitcoin to fund the dividend on their preferred shares. Having previously advised investors to sell a kidney before selling Bitcoin, this change of narrative has seriously damaged sentiment. If the big investors flip from bid to offer, the share price always goes down.

Medium Term Risks - the New zAIbatsu

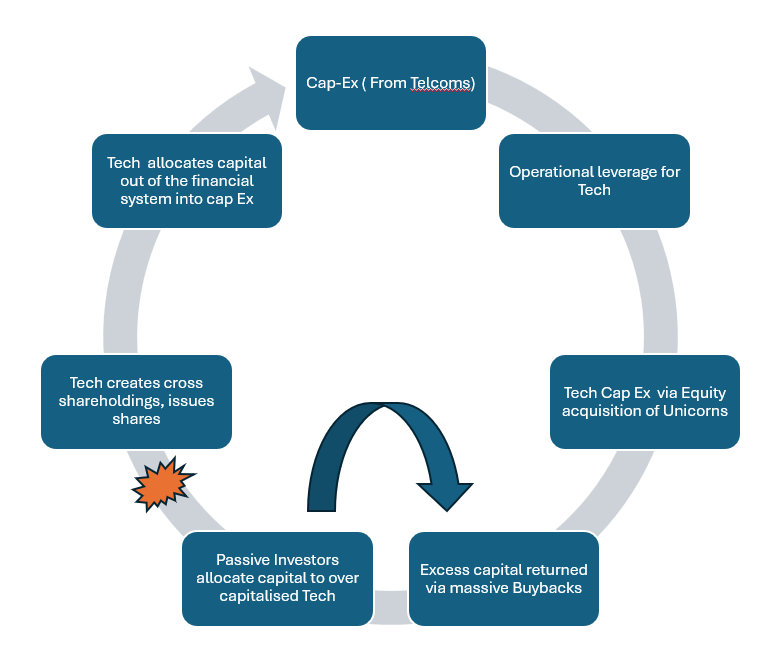

The medium term risks are thus those we discussed back last October (see the New zAIbatsu) as high margin capital light software companies transform into lower margin, capital-heavy AI hardware owners.

Over the last decade, Alphabet spent $342bn buying back its own shares. It has now just asked for some ($80bn) of its money back

Here is the image from that previous note, highlighting how the previous Capital Investment from Telecoms had delivered a ‘free ride’' for what has become the Mag 7, benefiting from a perfect feedback loop where the same mechanics now being used to fund the IPOs- passive funds buying based on market cap - were supporting share prices as cash flows were recycled into share buybacks and creating the tech Oligarchy.

Now we are seeing that loop broken - cash is coming out of the closed financial loop and is driving real world inflation - a lot of which is now being captured by a different part of the market - the whole switch from tech software to tech hardware is based on dramatic jumps in earnings for Micon, Sandisk, Intel and of course Samsung, SK Hynix and TSMC.

Structural High Margin Software companies are shifting to lower and more cyclical margin Capital Intensive Industrials

The listing of Space X, but also Open Ai and Anthropic it will also start to impact on the earnings of the Mag 7. Microsoft for example owns 27% of Open AI, having invested about $13bn so far. If the stock floats for around $1trn, then that’s a 17x on their investment, except it will be very difficult for them to sell any of it straight away due to regulatory and other reasons. They will however, likely sell it down over time to fund their own AI related expenditures, meaning a stock overhang. At the same time, they will have to account for the ongoing cash burn from Open AI. The temptation to offload stock will be high, adding to the insider (is) out environment likely to emerge soon.

To the extent that part of the support for markets has been the investment profits booked for illiquid holdings, this will now require accounting for the share of losses on the p&L

Softbank is a prime example as well. It owns a further 13% of Open AI, which they recently valued at $80bn, the mark up on their balance sheet briefly pushing them to become the largest company on the Tokyo Stock exchange. When it floats, they will have to adjust their earnings. To the extent that Quant models trade on headline earnings numbers (or their rate of change) this will be another example of mechanics flipping into reverse.

Amazon and Alphabet (Google) meanwhile are in a similar position with Anthropic. Something to watch, as earnings downgrades can trigger a different set of rules based systems.

Long Term Trends - AI as a major disruptor

All of the short and even medium term issues for the market are tied up with AI, which of course is long term story. Sure, we can use AI to generate the title image in a matter of seconds and, while that is fun, I am not prepared to pay much money for it (in fact Google Gemini did it for nothing). Indeed, the programmes like Sora that produced a flurry of (expensive) high quality video output that suddenly filled YouTube with PanVision retro versions of Hollywood movies have all quietly been dropped and, for us at least, the growth is more in areas like Robotics and automation.

Which raises questions about the total addressable market for AI. Musk says $28.5tn, which for context is around $4000 per person for the entire world. If you focus on the so called Golden Billion in the west, that is $28,500 per head, an obviously ridiculous number. More magical thinking, requiring Wall St analysts to try and earn their share of the $1bn fees to twist their valuation logics to the extreme. There are also echoes of activities pre IPO for stocks like Uber, where huge ride volumes were generated from ultra low prices as volumes, like clicks, were the metric being measured (and thus managed).

If we step back and look at the process that got the Mag 7 where they were most recently, it was that the products they created sat on the back of infrastructure that they didn’t pay for, just as happened with previous investment booms in Railways, electrification and industrialisation. Forecasts of future VodaFone revenues made in 2000 were not far off, it’s just that they ended up being valued on 0.8X Sales rather than 8x.

We can see how AI can transform smaller businesses - the operational efficiency gain with one smart analysts and 30 AI Agents is far greater than the saving of swapping 20% of an existing large analyst team for AI - but for larger organisations, the institutional inertia looks too big. The boss class might like the excuse for what is essentially a hiring freeze/layoffs, but, as is always the case, the people you need are most valuable to the smaller competitor looking to upskill.

Evans’ law says that in any large organisation, the square root of the number of employees do half the work. Unless it’s them making the decisions, it’s unlikely AI will help

Ultimately, it’s about the economists’ concept of a Producer Surplus or a Consumer Surplus - who gets the excess return? History tells us that competition ensures that it is always the consumer, even if, as with the MAG7, the consumer is another corporate - which serves to drive down margins for the incumbent.

AI is great for system architecture, enabling small businesses to get the benefit of scale business, without the cost. As such it is going to be tremendous for competition - good for the consumer, if not necessarily share prices of large corporations. This is what the market was starting to tell us is the SaasPocalyspe earlier this year.

As a real example, we can use Claude Code to build a CRM system for almost nothing. It won’t be as good as the Salesforce version, but as a small business we would not have bought that anyway. But if we need to expand/upgrade the likelihood is that another middle man can offer something almost as good for a much lower price.

As for the Bloomberg terminal…..

In the light of this, S&P’s decision not to include SpaceX in their benchmarks any time soon (unlike NASDAQ) may be upsetting the passive will be buyers narrative a little ahead of next week