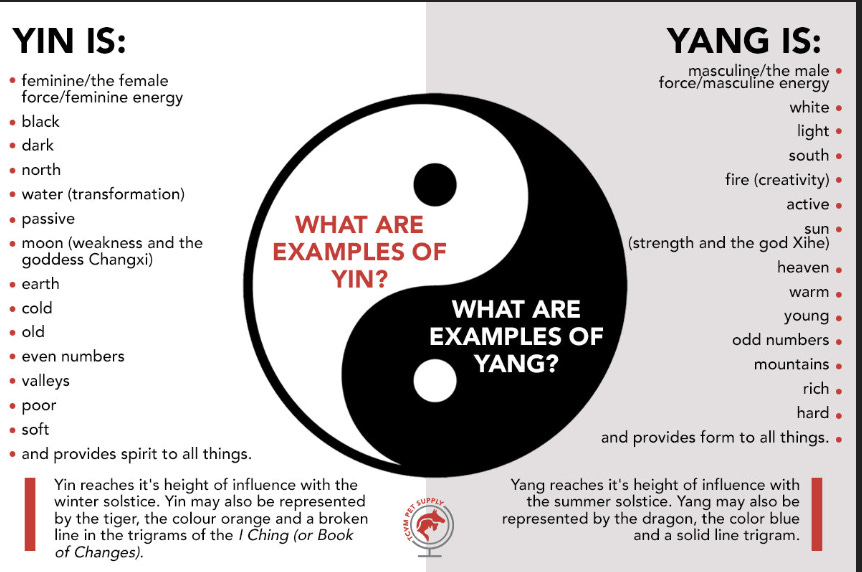

Yin and Yang

Stage 2 thinking in thematics

The Chinese symbol shows that for every Yin there is a Yang, male and female, light and dark, active and passive, fire and water, sun and moon. When we look at Thematic investing we often find that this 3000 year old philosophy is helpful, there are both opportunities and threats to most of our themes. They are opposite yet connected. For example:

Worrying about Demographics and also worrying about AI and Robotics is to ignore that one is a solution to the other. You don’t have two problems, you have a problem and a solution.

Autonomous vehicles are a threat to taxi drivers but will solve for a current shortage of truck drivers and reduce the need for car parks, delivery drivers, congestion, energy usage and transportation costs.

Building out data centres for AI is driving commodity prices and cyclical inflation, investing in AI means also investing in mining stocks and rare earths.

But ultimately AI is deflationary. The biggest sources of inflation in the US over the last decade have been health and Education. Both are going to be disrupted by AI, which will improve output and reduce costs.

Meanwhile, excitement about quantum computing implies the need for an equal focus on Cyber Security as the former will create unprecedented demand for the other.

Space is now central to the defence industry, but also to communications, mining and energy. Developing one will lead to developments and threats and opportunities to the other.

The great Economist Thomas Sowell often refers to Stage 1 thinking, the simple layer too often embraced by politicians that takes no account of second order effects. Consequences may, seemingly always, be unintended, but they are rarely unforeseeable. Thus, when looking at evolving themes and sectors, we believe it is sometimes important to link them together as one being the stage 2 of the other.

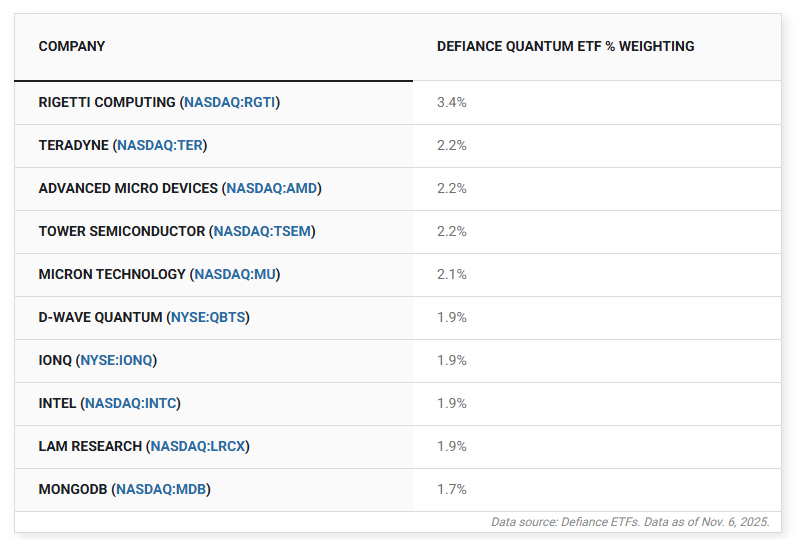

For example, excitement about Quantum computing led to a scramble last year to find stocks (and ETFs) to participate in this new and emerging theme. When looking at a list of stocks, as, for example, here, we see a list including the usual suspects: Microsoft, Nvidia, Alphabet, Honeywell and IBM, with only IonQ offering any diversification from an existing portfolio.

The ETF mentioned elsewhere in the same linked article offers some more diversification in names, which is how we prefer to invest in themes (albeit we use UCITS compliant names) without taking too much stock specific risk, but also without simply ending up in big mega caps names for which the theme is a tiny proportion of their earnings.

Please note, as always, none of this should be considered investment advice.

However, the excitement about Quantum also triggers interest in something else, the Yin to its Yang if you will, which is an undoubted need for Cyber security. An obvious risk from developing Quantum computing is that it will make obsolete most existing Cryptography, simply through its ability to do eons worth of calculations in a matter of minutes. Already there are risks that adversaries can ‘steal now, decrypt later’ and the US Government is clearly flagging this as an issue.

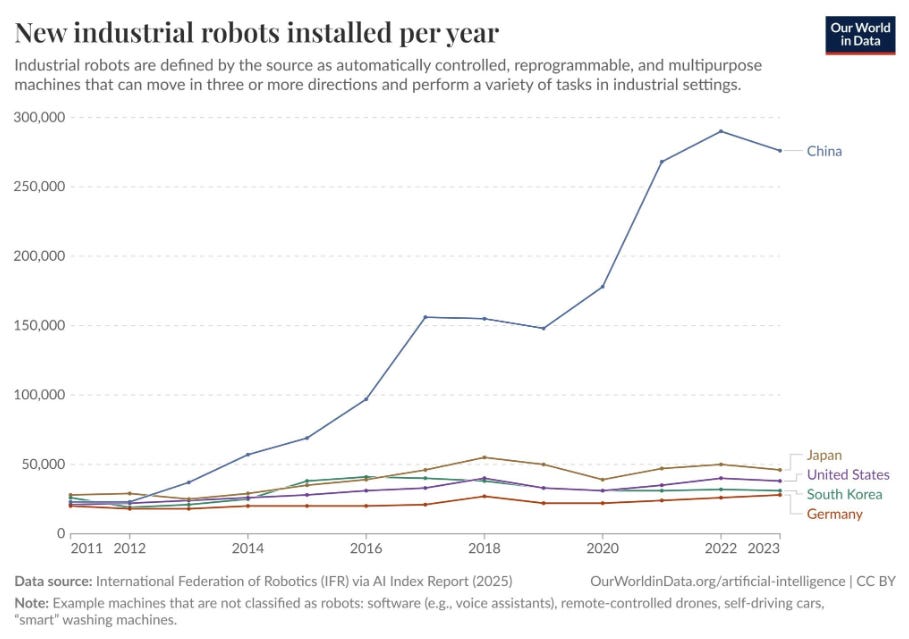

If those two are opposite sides of the same thematic coin, then AI and Robotics are the hardware and software aspects of the same trend. Robotics has been a favoured thematic for over a decade (with our previous employer we worked on a Robotics and Automation fund that was one of the early single theme funds), but rather than switch to the AI theme, we now like both - albeit like most things with a much heavier China tilt these days. Perhaps not surprisingly when you consider the graphic below.

The next stage of Robotics is obviously Humanoid Robots with a significant overlap with the EV space. After all, an autonomous car is essentially an AI enhanced Robot and much of the systems, parts and software are common to both. Currently, around 70% of a Chinese EV is built by Robots. Of the remaining 30% of that, much could be built by humanoid Robots.

Robots, humanoid or otherwise, are also stage 2 thinking at a macro level. One of the ‘risks’ we are always told about China is that its population is shrinking (it was a risk when it was growing as well of course according to the same western experts), along with Japan and Western Europe. In part this taps into the stage 1 thinking about open borders that was embedded into economic models that conflated immigration with GDP growth while ignoring GDP per capita.

A shrinking population, we are told, means fewer workers to support the aging population, but if AI and automation make those workers twice as productive, what is the problem? Two hundred years ago more than 50% of the population worked in agriculture, now less than 2% do. Technology feeds more people - with fewer people.

This is true across the board. Consider the charts from the FT showing the shrinking in manufacturing in the US.

Eagle eyed readers will have spotted the transportation and warehousing on the right hand chart, which is largely a function of the internet delivery economy and is another ‘great worry’ about AI. Autonomous vehicles will challenge one of the biggest employment sectors, but then again the real issue is that there are currently not enough truck drivers. According to Transport Insights:

The average age of truck drivers globally has risen to 44.5 years, a trend that is likely to worsen as more drivers over 55 retire in the coming years. The report estimates that 3.4m truck drivers will retire over the next five years, with 21% of drivers in Australia expected to retire by 2029, 18% in China, and 17% in Europe.

Thus, two of the things we are supposed to worry about actually solve for each other.

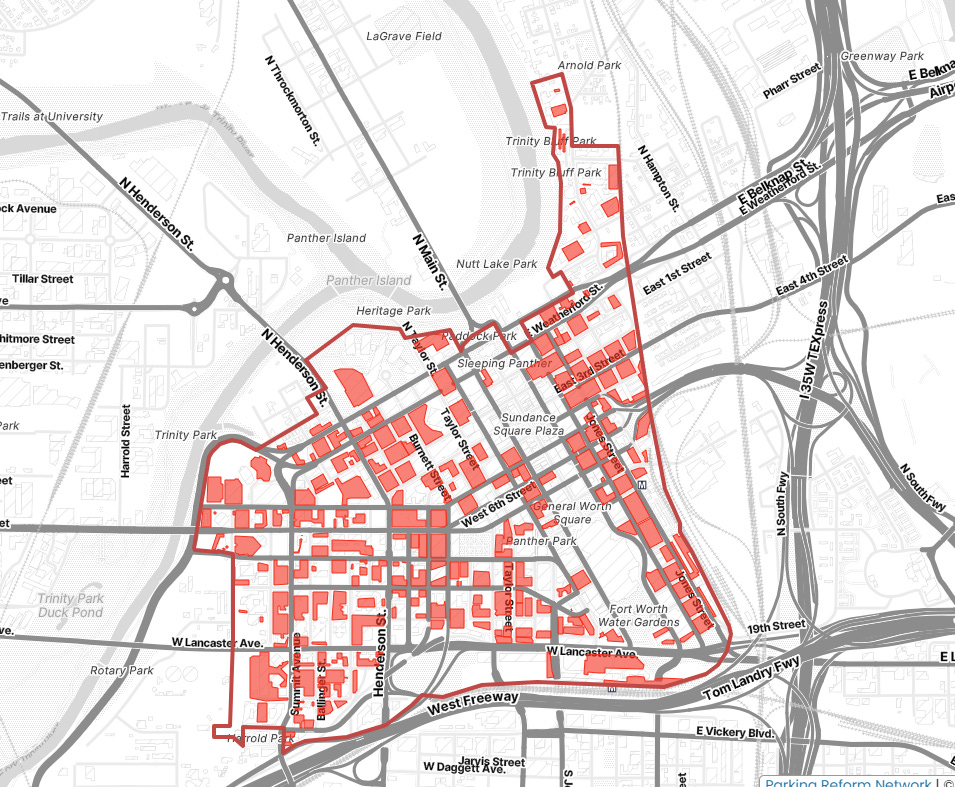

Autonomous vehicles will also help solve for a variety of other ‘problems’, most notably public transport and parking. In the US, large amounts of urban centres are taken up with car parks, where capital equipment sits idle for most of the day.

In Fort Worth Texas, 29% of the central City is off street parking.

The map comes from a great (if a bit geeky) website that can show the % of city centres taken up with off street parking lots (note, this does not include underground). Every city is on there and ranges from New York (basically nothing) and Washington DC at 4%, to San Bernadino in California at 49%, with an average in the 20-30% region.

Positive Social impact from AI and autonomous driving.

What if you drive to work and your car drops you off and goes home and comes back when you need it? Or it goes and collects the shopping you did online and then works as a taxi during the day until it is time to pick you up again? Maybe you have a time share in a car with one or two others whose schedule works for you all.

Maybe it can sell the power from its battery that it charged overnight to a business that needs it during the day? Conversely, rather than sitting in a car park, maybe it can go to a solar charging point during the day and power your home at night?

Yes, it might make some taxi drivers redundant, but the fact that transportation is one of the biggest costs for many households - in the US it averages 17% of spending, mainly for purchase and maintaining personal vehicles - means these innovations can and will free up income to feed growth elsewhere in the economy.

The point of advances in technology is that they are there to solve a problem that has been identified. Thematic investing tries to focus on the solutions, not dwell on the problem.

Part of the appeal of this balanced approach to us as investors, is that we are basically in the world of Equities, the active world of the Yang, while we see Bonds as more in the passive world of the Yin. Bond investors focus more on downside risk while Equity investors can look at potential upside - which is more fun obviously.

Also obviously, as portfolio managers we recognise that both work together. Currently, the markets have picked up inflation (bad for bonds) but also on the commodity and metals theme, not just the monetary metals of Gold and Silver, but the industrial metals, most obviously Copper.

For illustration, the chart shows how, since the mid- November dip in markets, the Global X Copper miners ETF is up over 50%.

This is not to recommend a particular ETF (Reminder none of this should be considered investment advice, do your own research and always talk to your financial advisor) rather to illustrate the point that the cycle is not dead and businesses with high fixed costs and apparently low margins can deliver explosive earnings per share growth when operational leverage kicks in.

Consider a simple illustration; A business with a 10% operating margin where fixed costs are 70% and variable costs are 20% sees a 5% increase in sales. On $100 of sales it makes $10 of profit, but on an increase to $105 of sales its variable costs only rise from $20 to $21, so its profits jump from $10 to $14. A 40% increase.

That is the beauty of cyclical stocks and why top-down forecasts of profits based on GDP are often so out of line. However, we should also make the point that for long term themes such as the supply demand imbalance for copper to make investment sense (this is hardly new), they need to coincide with a narrative shift, which is often as the operational leverage starts to come through in the earnings.

As to the demand side, the situation was summed up beautifully at a recent conference by mining entrepreneur Robert Friedland:

“To maintain global 3% GDP growth, we have to mine the same amount of copper as we mined in the last 10,000 years combined”

Robert Friedland

And that is without the demand from electrification and the greening of the world economy (!) The substack linked here has a great digest of Friedland’s comments, not only on Copper but also on critical minerals in general, but the bottom line is that in order to thematically ‘invest in AI’, stage 2 thinking has us also investing in Copper miners and rare earths.

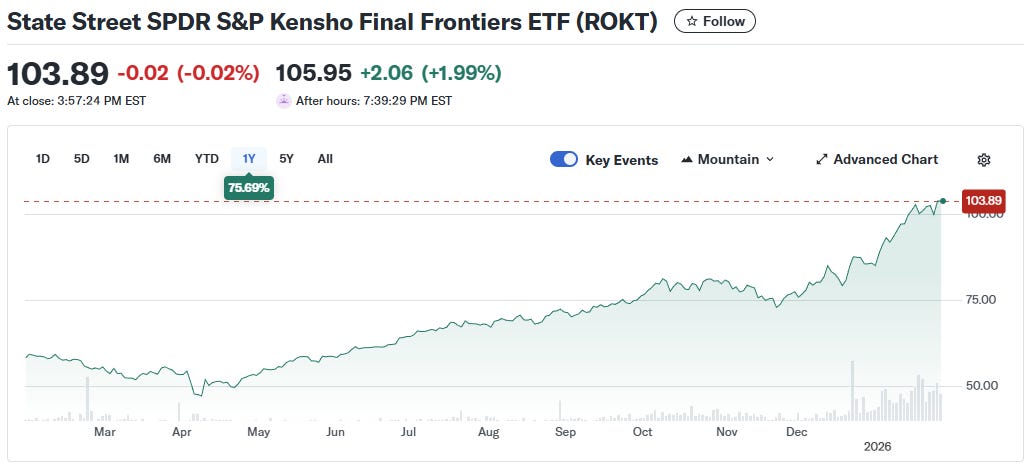

Finally on Space - another thematic that has gone parabolic recently and another ETF for illustration only.

Thematically we - and clearly others - have seen Space as a way of playing the future of defence, having seen the way the conflict in Ukraine has evolved, but as Elon Musk pointed out at Davos, it is also potentially the future of Energy, with plans for SpaceX and Tesla to produce 100 GW each of PV per year. Importantly, and being Elon Musk, he talks about this happening withing 2 years, meaning that this is not like Fusion or other potential energy disruptors. Space based Solar Power is being actively pursued by multiple governments, as evidenced by the graphic from this report.

China, Russia, the US, Germany, UK, Japan are all there.

Bottom Line

We have always seen Global Thematics as the best way of diversifying a long-term growth portfolio, but recognise that simple, stage 1, thinking is not sufficient, the Yin and the Yang are equally important for a balanced portfolio, bonds and equities, growth and income, risk and return.

When Yin is strong, it contains Yang. When Yang is strong it contains Yin

As investors increasingly seek to diversify away from the heavily tech-concentrated world of passive investing they are essentially moving from Passive Yin to Active Yang. Investing thematically helps take that to the next layer down, finding winners, but avoiding losers and thinking about how one winner can create another. And of course, vice versa.