In his Nobel Prize winning book, Thinking Fast and Slow, Daniel Kahneman points to the different functions of our considered and thoughtful slow brain compared to our rapid response fast brain. The former might consider the fact that 90% of the time there won’t be a lion in the bush behind you, but the latter uses quick rules of thumb known as heuristics, often as ‘risk management devices’ – that noise from the bush probably isn’t a lion, but on the basis that if it is, then I am dead, it is probably best to take evasive action.

So it is with markets – which is a key reason why we look at short-term traders (fast brain) differently to medium-term asset allocators and long-term investors (slow brain) and why Thinking Fast and slow is one of our favourite books.

April was a classic fast brain month, the slow brain knew that the tariffs were coming, but the risk management that kicked in at the end of the first week (we believe mainly from the large multi-strat hedge fund complex) threatened a cascade effect in an already fragile market. Fast brain response kicked in as books were flattened and this saw traders selling what they could, not what they wanted. It also created a scramble to close short Treasury positions in fixed income – causing credit spreads to blow out – and then saw those bond yields ‘flip out’ again.

The action of Gold was relatively slow brain, but for international investors the Dollar was not. It has fallen 10% from it’s January peak, triggering a lot of fast brain covering and rapid switching into non US assets.

As we described in Unknown Unknowns, there were also tensions in the repo markets creating liquidity shortages and market heuristics saw the shadows of lions – the 2018 repo mini crisis, the 2020 distressed selling, the 1998 LTCM crisis, 2008 and even (for some of us older investors) 2000, 1997 and 1987. The response was to cut and run to cash.

By the end of the month, the NASDAQ and the S&P were back to their levels at the start of April, which looks largely to be down to US domestic retail inflows, meaning that for many investors inaction paid off.

Except that beneath the surface a lot has changed. The slow brain activity is now kicking in such that we believe May is going to be a start of some significant rotation as the asset allocators start to diversify out of US$ assets, just as the traders have done.

Short term uncertainties

Traders went into April already reducing risk, such that markets were quite fragile and were swift to cut positions further as the Trump tariffs triggered some heightened uncertainties around the internal dynamics of markets themselves - notably in the Repo Markets. The dramatic moves were seized on by economists and politicians alike as ‘fundamental problems’, but we would suggest that is to confuse fast brain and slow brain. This looks to us for all the world like ‘market mechanics’.

Treasury Secretary Bessant understands the plumbing in a way his predecessor never did and was likely the reason for the ‘pause’ in the rhetoric, but again, we see little evidence that the Trump administration is going to ‘give in’ to Wall Street demands to keep a gravy train rolling.

It looks like US retail have come back in to NASDAQ and the S&P, as their particular heuristics focus on ‘buy the dip’ with a reference time frame back around 5 years in many cases. However, we suspect that the professionals are more wary, looking not only at a longer time frame of reference, but also considering the slower brain behaviours of the asset allocators - the ‘Big Money’ that they are always trying to nudge in support of their existing positions.

The big uncertainty is around whether this is a bear market rally in US Equities or a resumption of a bull market?

Sometimes referred to as ‘Dumb Money’, the Big Money is in fact nothing of the sort, it just has a different set of risk/return expectations and requirements. Traders are always trying to ‘get ahead’ of the big money flows and obviously try to steer the narrative as much as possible, but are always wary if they sense the flows are about to shift.

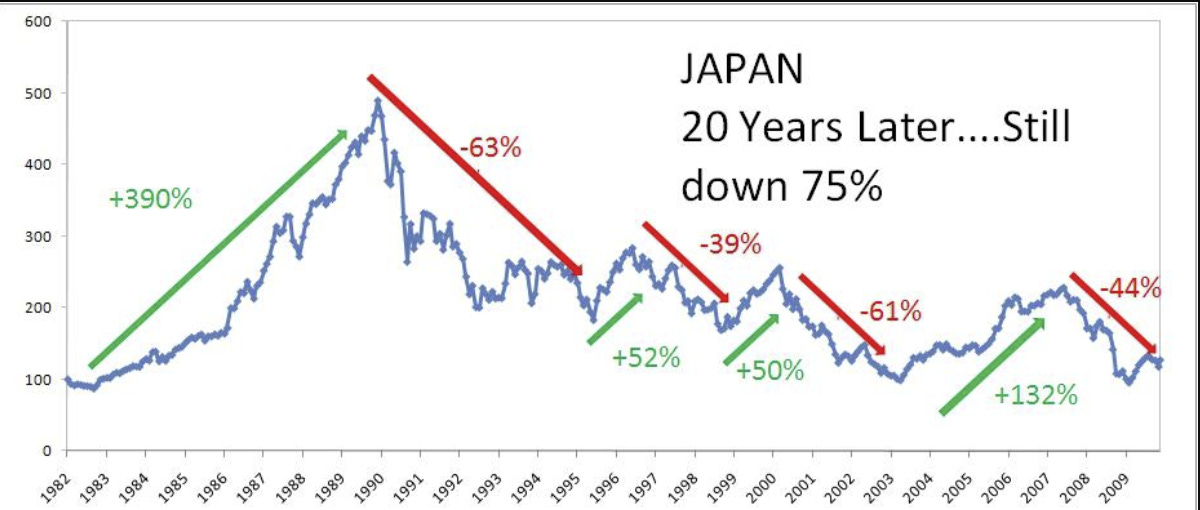

In this case, we think they are looking at a potential major reversal of flows into US assets by International investors that would mark the end of an asset-allocator bull market, similar to what happened in Europe and the US in 2000 and also in Japan in the early to mid 1990s.

This is the analogue to worry about for buy and hold investors

To be clear, the use of analogues is illustrative rather than formulaic, but look at this screenshot. At its peak, the Japan market was the largest in the world and many international investors had almost half of their holdings in Japan ‘to minimise benchmark risk’. Similarly in 2000, UK investors had 14% in Vodafone and European Investors 10% each in Nokia and Ericsson, again to minimise ‘risk’.

It’s the hope bear market rallies that kill you*.

We note that in the case of Japan. the bulk of the selloff from the peak happened in the first two years, but look at the destructive power of the two decades of bear market rallies - dramatic short term rises followed by soul destroying drops that led to lower lows and lower highs each time. (* as Mae the barmaid almost said to Ted Lasso).

As we remember from the time, it was possible to make great returns from Japan in that period, but you needed to have a dynamic rather than a passive approach,

Medium Term Risks

The markets may have stabilised somewhat with the headline numbers even up slightly on the month, but the movements beneath the surface have changed. We thing permanently.

The Asset Allocation meetings that drive the Slow Brain, Big Money, decisions will now be focused heavily on diversification – if they weren’t already. Most Year-Ahead notes had commented on the risks embedded in having almost 70% of Global Equity exposure in a small handful of, highly correlated, high-beta US tech stocks that were also heavily owned by momentum investors, but equally many, even most, Big Money investors were dragging their feet in reducing that risk.

It might be unfair to suggest that the real risk they were focussing on was ‘underperforming’ a benchmark that was passively taking those risks, but if that were the case, then it is much harder now to ignore those risks. Career risk has shifted and the slow brain is now also thinking of some heuristics; this could be like 2000 and the tech bubble, or even the mid 1990s and Japan. The chart above will be ‘top of mind’ for many of them.

As will the 2000 equivalent. Remember that the market sold off in March 2000, before clawing it back by October. Then it really went down for two years.

Career risk has shifted and echoes of 2008, 2000 and even Japan in the 1990s are focusing the minds of asset allocators

In particular, the selloff in the $ - likely at least in part to do with the capital reallocation already taken place – will be focusing the mind of international investors, many of whom had been buying NASDAQ as a new form of Treasury Bond.

Was it the SWF’s?

One thought that occurred to us is that instead of buying US Treasuries, a number of large family offices and even a Sovereign Wealth Fund or two have been buying a barbell of US cash and NASDAQ, while traders using leverage (and leveraged ETFs) have been doing likewise.

Selling those positions to reduce $ exposure would have had the effects we have just observed, including a sharp rally in Gold, but also in the Euro and European Equities but particularly the Swiss Franc and Swiss Government Bonds, which are once again offering negative yields.

We would note that the Swiss National Banks has famously been a large investor in NASDAQ rather than Treasuries, with up to 25% of its Foreign exchange portfolio in equities. So perhaps it is the gnomes of Zurich reducing $ exposure by selling US Bonds for Swiss bonds and US Equities for European Equities?

With a paradigm shift in tariffs and hence the need to manage Foreign Currency reserves differently, there will likely be a shift in the demand for all $ assets

Of course, when the Swiss Bond Yield goes down – and even becomes negative- it is explained away as a flight to quality and a bet on stability, but when the Chinese Bond market does something similar (Chinese Bonds were one of the best performing bond markets globally last year) it is explained away as ‘China is collapsing and is in a deflationary spiral’. To a man with a hammer etc.

It may well be that the Chinese were also selling NASDAQ to buy Gold and other non $ assets. Indeed, for all the conspiracies that the Chinese were dumping US Treasuries (which we don’t believe) it would arguably be more ‘effective’ and disruptive to dump the NASDAQ if they were thus inclined.

Again we don’t think they are, but the actual message from the US appears to be that they don’t want trade surpluses being recycled into US Financial markets, they want them to invest in real assets instead. But obviously not China.

China is thus likely to recycle its dollars elsewhere and as we discussed in Not to de-dollarise but to re-dollarise, that could actually mean lending US$ to other countries and even issuing US$ debt to then lend on to other countries. In effect it could take over the offshore US$ bond markets. The ultimate IP theft!

Instead of lending its surplus US$ back to the US, China could lend them itself to the offshore Euro$ markets.

Generally though, we believe that the diversification strategies of the Big Money will start to become more nuanced, driven as they will be by a new diversity in monetary and fiscal policies. Thus instead of the Fed setting world interest rates and Emerging Markets operating as a Bloc using an index created by a passive investment process, we are thinking about a mix of new markets where a modest passive index position can capture broad market beta, but size and market cap is no longer the method of portfolio construction.

Long Term Trends

We see the Trump Tariffs less as a trigger for the April selloff and more as a signal of a change in the tides. As we described it last month, we see investing as like sailing, when the wind, the tide and the currents are all aligned then things are ‘easy’. As and when the wind shifts, we can get choppy waters, but we can largely resume course after a bit of tactical ‘tacking’. However, if the choppy waters are less because the wind has changed direction and more to do with a change in the tide, then we need to plot a new course.

This is where we think we are now. We see the tariffs as a continuation of the Obama era policy of TPP without China. The aim is to have the so called ‘Golden Billion’ of ‘The West’ in a form of Customs union behind a giant collective ‘Blue Team’ tariff wall against the ‘Red Team’ of China and the BRICS, while keeping the Red Team divided by offering side deals.

Meanwhile, the old business model of US multi nationals manufacturing offshore and using transfer pricing to avoid tax is coming under increasing scrutiny - indeed we see this as a major target of the tariffs. This is not a new issue, but previous attempts to tax the Multinationals have been tied up by lawyers or frustrated by lobbyists.

The OECD has issued proposals on Global Minimum Taxation which were agreed by over 130 countries and would seek to capture some estimated $150-250bn of tax, but, as noted here, the Trump administration is rejecting the argument.

We would suggest that it is because they see the key point of the tariffs is that they bypass this transfer pricing such that most of the tax will end up in the US. If you want to manipulate your cost of goods sold by charging a high input price from your offshore subsidiary, you will get caught by tariffs. Charge a normal price and you will earn higher taxable profits. Heads you pay tariffs, tails you pay tax.

This is likely a powerful lever on the EU, which gets little benefit apart from some ‘head office’ jobs but will now perhaps get tariff reductions in return for co-operation with the US tax authorities.

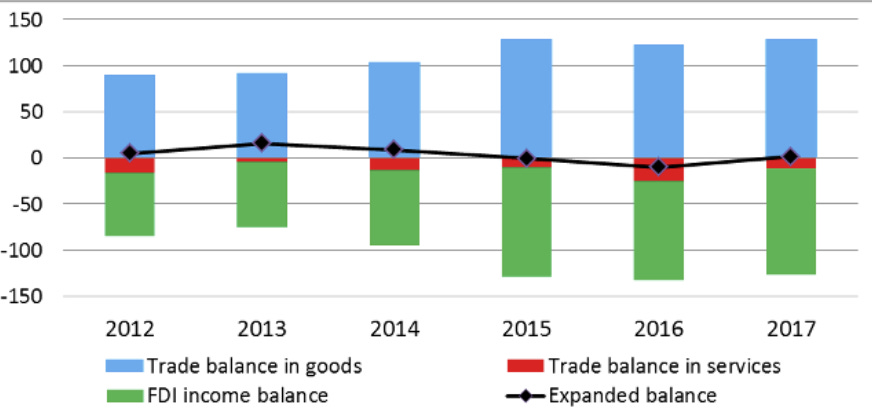

As this Bank of France article from 2017 points out, the actual EU trade imbalance with the US is almost entirely removed when accounting for the activity of US Multi nationals via the FDI income balance. Most of this is in the Netherlands, Luxembourg and Ireland. No wonder Grant Thornton are merging their US and Irish businesses.

Take out the US multinationals and there is no ‘unfair surplus with the EU’

Source: Bank of France

We see this as meaning all US multinationals paying 15% or more ‘tax’ to the US Treasury, either via tariffs or via ending transfer pricing and paying more ‘normal’ levels of Corporation Tax. Given that this likely means lower distributable earnings (and by extension fewer buybacks) this would add further reasons to diversify away from US mega caps.

Meanwhile, the suggestion from US politicians that the US de-list the Chinese ADRs, apart from being a self inflicted wound (the companies already have their capital) should be good for Hong Kong as it would be the obvious place to ‘re-list’ the companies that are currently only available in the US (around 25% of the total). Putting them in the Stock connect scheme could help ensure liquidity, but it would also re-focus attention on the Hang Seng as an alternative home for international investors looking to diversify some of their capital away from the US.

Please note that none of this commentary should be taken as investment advice. Please do your own research and speak to your financial advisor.