Rough Waters subsiding

April Market Thinking - Correction not Collapse - but tides may be turning

We often compare investing to sailing; investors can sit in safe harbour (cash) or they can venture out in most, if not all, weather. Sometimes it requires a lot of tacking and trimming sails to seemingly achieve very little as the winds and tides fight each other, sometimes it is, as they say, plain sailing and the best thing to do is stick on the same course.

Obviously, and to extend the metaphor, fishing boats need to sail to where the most fish are and sometimes that means going to places where the weather is less predictable.

The decision for the fund manager/Captain in these waters is then about how to respond to sudden changes in conditions. Sometimes it makes sense just to lower sails and sit tight, at other times to return to harbour. In a diversified portfolio it sometimes makes sense to do a mix of the two, switch some trades to cash while holding others intact and using the cash to subsequently top up the trades facing the better weather.

That is essentially what we did during March, and the fact that we were diversified across geographies and themes definitely helped as the squalls hit the Nasdaq and the Mag 7, the areas where the majority of investors have been busy harvesting returns in the last two years.

We are still fishing, but sense more boats coming our way now.

As noted last month, risk appetite started to deteriorate at the end of February and March saw a correction across Global Equity Markets, focussed on the US, which is where almost 70% of the index weight resides. That of course was the problem (one that we discussed in our December Market Thinking as well as our Review/Preview year ahead note) that so-called low risk tracker portfolios were overly concentrated in a small number of highly correlated, high Beta, US tech stocks.

To adapt our fishing metaphor, the most fish were off the Mag 7 reef and so that’s where almost all the boats were. And that is where the squall has just hit.

We note that the Diversification call that we and other made at the start of the year was suddenly very much in fashion in late February and early March, with the US market peaking almost exactly 3 years to the day after the start of the Ukraine war and 5 years after the first outbreak of Covid in Italy was reported.

Once again, a lot of market mechanics are being mis-diagnosed as economics

Institutional Investors buying index puts triggered some ‘market mechanics’ as market makers scrambled to hedge their (Gamma) exposure by selling the underlying stocks, triggering a, now familiar, downward spiral. At the same time, the explosion in ETFs and options on ETTs has extended the gamma problem to ETF market makers, as a growing number of ETFs have large exposures to relatively illiquid stocks.

Market favourites Meta and Nvidia were both off double digit in March, while Tesla was at one point down by more over 25% - which, given the large amount of short dated options in the stock, will have caused a lot of distress.

Mag 7 investors are blaming Trump and Tariffs for the end to their winning streak

Overall the Magnificent 7 are down around 14% ytd and a lot of bull market investors are looking for a reason why. Their narrative on this is clear - it’s about Trump and it’s all about tariffs. We would disagree.

We would say both Trump and tariffs are important, but they are not the reason for the sell off.

Not very inflationary - and cost push, not demand pull

If it was really about tariffs, then the European markets should have been going down more than the US. But they haven’t. This is because reciprocal tariffs will likely hit Europe much harder than the US.

As we explained in welcome to MAGA-Vision, we can see the logic for US tariffs and as we noted in discussing Canadian tariffs, putting 10% on the $150bn of heavy crude imports from Canada will a) not affect Canadian exports and b) put no more than 5c on a gallon of fuel in the US (if that). They will, though, raise a helpful $15bn a year that goes straight to the US Treasury.

The same is true of Timber and aluminium, a 10% or even a 25% increase in the wholesale price of a commodity input will have a limited impact on the price of the finished good and thus the likely inflationary impact on the US consumer is likely going to be minimal.

We did get a rise in the price of various goods due to the supply shortages arising from Covid, but these were rightly regarded as transitory, as the higher prices brought forward a supply response. The real inflation problem came from the money printing during Covid - something that has since subsided. In the US at least, although the EU is threatening to turn on the printers again, this time based around an alarmingly ill thought out rearmament/industrial policy plan

Limited implications for US interest Rates

In line with this experience, the Fed has acknowledged that it would not raise rates if tariffs increased prices as this would (also) be transitory -cue howls of outrage from economists who continue to claim that the post covid cost push inflation was not transitory. Meanwhile producers such as BMW acknowledge that they would find increased tariffs very hard to pass on in a competitive market.

Tariffs may be worse for corporate profits than for US consumers

This second point is an important part of the calculus, for the real target of both the Canadian and the Mexican tariffs appears to be the export of cars and car parts into the US under NAFTA, not so much avoiding expensive wage costs (especially in the case of Canada) as avoiding other high employment costs, notably healthcare.

Indeed, it is ironic that what are often seen as restrictions on employment and growth in Europe - the high social costs in France, the high levels of NI in the UK - are effectively mimicked in ‘capitalist’ USA by the high cost of social benefits such as healthcare.

Of course, if the response from the Globalist ‘leaders’ in the rest of the ‘Five Eyes’ and the EU is to put tariffs on finished goods from the US, or on goods where there is no alternative supply, then they do risk their own version of ‘cost push’ rather than ‘demand pull’ inflation. Coming against a background of other imposed costs - employment taxes and green tariffs - this is deflationary (or worse stagflationary) rather than inflationary for Europe and the five eyes.

Tariffs are a from of cost push inflation, if there is no competition. In the US, Trump is cutting other sources of cost push, notably government regulation and Green tariffs. In Europe and the five eyes they are doubling down on existing cost push, while threatening reciprocal tariffs to make it worse.

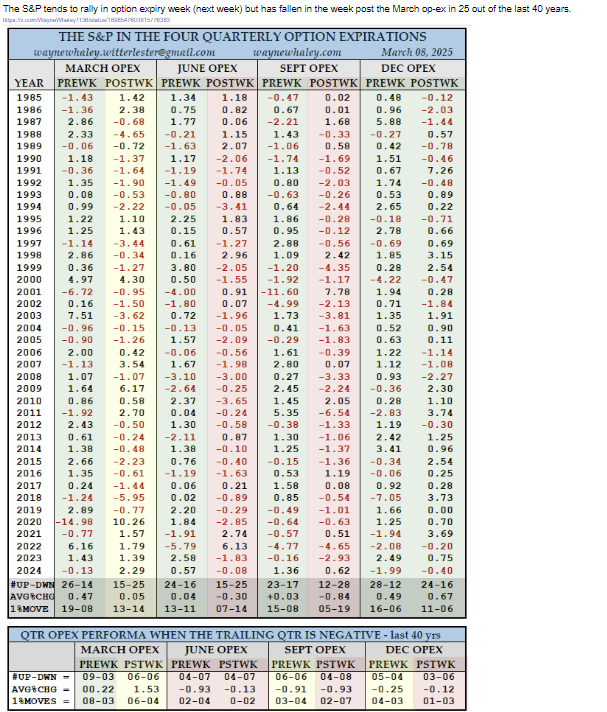

Muscle Memory for March

The table below, courtesy of our friends at Redburn Atlantic, makes the point that the week after March options expiry has been negative in 25 of the last 40 years, (63%), but having started work as a market strategist in 1987 and excluding the post Covid era, our financial muscle memory is nearer to 25 out of 33 years, ie 76% of the time.

Our explanation has always been that the asset allocators tend to use March options expiry to put on their ‘bets’ for the year and after a good Q1 will often buy puts running into the expiry, or vice versa. Hence our muscle memory is always to be nervous ahead of, what is often the Cheltenham race festival and/or St Patricks day (!)

And so it proved once again this year, although we have more substance to our actions, based on the behaviours of the Confidence Score cards that we use in our model portfolios and the DART fund that we run together with Toscafund HK (discussed at the top of the page)

Many of the more tech related ETFs we follow started to signal upcoming weakness, along with the Momentum Factor that we discussed in the March monthly, meaning that, while never trying to time the market, we nevertheless had been reducing exposure in these areas prior to the worst of the sell off, while sticking to areas such as Gold, Defence, European Financials, China Tech etc.

This is all part of the diversification trade

This is all in fact consistent with the trend we identified back in our year ahead piece of a need to diversify away from the huge concentration risk in the Magnificent 7 that had given great returns with a false premise of low risk.

Short Term Uncertainties - Still Team Trump Policy Risk

The discussions about Team Trump and their economics have unfortunately become heavily politicised, with not only the Globalist Main Stream Media (who remain almost universally negative) but also many threads on Linked in and other economic and investment sites are becoming clogged with personal opinion pieces about ‘Trump’ blending in with ‘expert economic and financial analysis’. This has added a lot of noise to markets.

As noted above, we recognise that Trump is bad for Globalisation and thus for the Globalists who have come to dominate the ‘elite’ in government, finance and the media (newly appointed PM Mark Carney being the poster child for this along with the unelected leaders in the EU). They are understandably the ones leading the protests against Trump and this it requires a careful parsing of their statements to see that they are correct only in so far as it applies to them and their interests.

What we do know about Trump 2.0 is that the focus is now on reducing the twin deficits - which can be good for bonds from a supply side angle but also because it risks deflation rather than inflation. Also that the earlier GeoPolitical trade of chasing the $ as a ‘play on Trump’ has now completely unwound and we are discussing the Mar a Lago accord and a weaker $ now.

Reversal of $ strength forcing thoughts of diversification

Obviously this is focussing minds on winners from a weaker $ like EM, Commodities and Gold. All of which have been running hard in recent weeks.

Trump is changing the weather

Trump 2.0 may well not be good for the overall US stock market as currently constructed since by definition it reflects the rewards under a previous, globalist, series of administrations - arguably back to Clinton. It can however be good for certain stocks and sectors that may now see favourable tail-winds or that have either been held back by unfavourable headwinds.

Thus to return to our sailing metaphor again, the fishing fleet needs to disperse and not all be sat on the M7 reef. Diversification away from US $ assets is the best risk management tool that many smart investors see right now, making Global investors more, actually, global.

The irony is that the dominance of the Globalists lead to a dominance of US Equity Markets. As we become less globalist, we are becoming more global

Medium Term Risks - AI trade unravels, European Bonds

To stick with our sailing metaphor, things can get choppy when the winds and the tides start to move in opposite directions and then when the wind drops and things appear to stabilise, the tide can start to dominate and push us in a, perhaps, unexpected direction.

This is our concern for the AI stock narrative. We are not alone in our concern over the ‘AI as Internet’ analogue, being old enough to remember not only the rise and fall of US stocks like Cisco and Sun Microsystems but also the dominance in Europe of stocks like Nokia, Vodafone and Ericsson. The narrative on the internet was incredibly powerful at the time, just as AI is at the moment, and ultimately (very) correct, but the peak of the markets saw the winds of momentum overcoming the tides of valuations and fundamentals. Until the winds dropped.

Something we discussed last year (in Butterfly wings and lightning strikes) was how what initially appeared to be a small disruption to the supply chain in mobile phones spiralled into a series of profit warnings for Ericsson and Nokia as issues such as vendor financing, concentrated supply chains, dependence on a small number of (often connected) counterparties and issues around cap ex and debt came to the surface.

Coreweave is sending up red flags for AI stocks - not so much AI itself.

The obvious parallel we saw was Nokia and Nvidia, not least because of the power of the narrative, which we acknowledged was (in this analogy) the wind overcoming the shifting tides and thus was ‘too early’ to call. Now it seems less so and that is because of the ‘news’ out of a small and relatively obscure company called Coreweave,

We have watched Coreweave for a while now and the, shall we say, ‘less than successful’, IPO of CoreWeave at the end of March has set up a series of potential red flags for us. Not just for the stock, but for the wider market (as ever, please note none of this is to be considered investment advice. Please do your own research and speak to your investment advisor) .

The full (worrying) details about Coreweave are given in this excellent substack post from Ed Zitron which we would highly recommend reading but the TLDR is that:

Coreweave is a major supplier of outsourced capacity to train AI

as such it is a major customer of Nvidia, owning hundreds of thousands of its GPUs, putting it just behind the hyper-scalers in terms of capacity

over 70% of its business comes from a single customer, Microsoft

it has contracted to build out enormous amounts of capacity, seemingly via a third party called Core Scientific which used to be a bitcoin mining operation

that commitment requires a vast amount of capital that it doesn’t have and it is already drowning in debt

Its senior management have been cashing out while it has yet to make a profit on a business model that seemingly requires $140 cost for every $100 of sales

This sounds worryingly similar to the problems that Nokia and Ericsson encountered in 2000. The rush to scale meant supplying vendor finance to customers whose ambitions exceeded their financial capacity as well as the recognition that their own sales number expectations might not only therefore be inflated but that the multiple the market was placing on those sales needed to shrink.

Nobody was wrong about mobile phones and the internet, but within 2 years of the March 2000 disruption in their supply chain, Nokia’s share price was down 75% and Ericsson’s by 96%

Second. We have been fans of the European Financials thematic for a long time - inspired by our former colleagues at Toscafund in the UK, who, as financial specialists, had identified that, almost uniquely, European Banks were going to be winners rather than losers from rising interest rates. (We discussed this in more detail in a post ‘Solid silver at Sohn’ back in May 2024, a year after we picked Italian bank BPER).

Unable to put their fund structure into our own UCITS fund, or pick single stocks, we instead bought into the Beta via an ETF and it has still proved a great investment.

Our process is designed around behavioural finance and watching how the three key players - long term investors, medium term allocators and short term traders are acting, European financials has been a classic example of long term buying in first and only recently have the allocators joined in (the traders come and go, largely reflecting momentum). Thus at the moment, all three are in the same direction, positive, but we admit to becoming slightly nervous about the medium term risks, for European rates are now falling and the value aspect of the trade, while still there is less compelling.

In particular, we are watching for the European Bond markets, feeling uncomfortable about the politics and the posturing - particularly around breaking the Budget for defence spending.

Unlike the AI trade, this doesn’t yet have a catalyst and the diversification trade is clearly still a supporting tailwind, but it is one that we are watching closely.

Long Term Trends - less Globalist, more Global

The Trump Trade is really part of a long term shift in Economies. We noted back in January that there was going to be a fight as Team Trump threatened a wide range of vested interests and right now the biggest push back is coming from ‘allies’ in Europe, and the so called ‘five eyes’, especially the UK and Canada, where the Globalist influence remains very strong.

Investors are just starting to take notice and the asset allocators are diversifying out of an overly concentrated position in US$ assets. If the US $ itself starts to decline then this will obviously accelerate. In recent years a lot of Sovereign Wealth Funds have switched from buying US Treasuries to buying the S&P500 instead, riding a relatively low volatility, relatively low drawdown up trend. If, as and when, this turns, then a significant part of the S&P500 ‘bid’, which importantly is both value and stock agnostic as it is simply replicating a market cap weighted basket, will disappear.

We are wary of drawing too tight an analogy with the post dot com era, but, as discussed above, when the tides turn, then some, often unpleasant, features are revealed and investors re-allocate quite aggressively. Warren Buffet’s famous line about when the tide goes out (you can see who is swimming naked) dates back to the late 1980s after another bubble of sorts ended in the 1987 crash.

The irony is that the era of Globalistaion, particularly after 2008 when it was combined with QE and ultra low US interest rates, lead to an increasing dominance of one stock market, the US, as US corporations were best placed to exploit a combination of access to ultra cheap capital and a lack of barriers to entry in emerging economies. In addition, rules and regulations were shaped to benefit large, semi monopolist companies at the expense of smaller institutions.

China, and some other economies, grew rapidly, but their stock markets did less well, leading to a false conclusion that one should lead to the other. In acknowledging that the US needs to compete, especially with China, Team Trump is shifting the policy priorities and while that may be good for some, on balance it is unlikely to perpetuate the high ratings for the winners under the system now being changed.

By contrast, we see that China is now looking to develop a more efficient set of capital markets for both long term savings and investment. Just as the US took over from Japan as the world’s largest stock market in the early 1990s, so we see it entirely possible that Asia, and China in particular, can take over the next phase in capital markets, especially if the US $ begins to weaken (deliberately or otherwise).

The flip side is that perhaps, the US responds to the current situation by becoming more like Asia (!) By this we mean something like a new Sovereign Wealth Fund allocating capital - likely as a co-GP with the giant PE funds - to build efficiency enhancing infrastructure. This would of course likely trigger a new commodity super-cycle. Something that the recent behaviours in commodities and industrial metals may already be hinting at.

As such, the overall long term result of Trump taking on the Globalists is that investors need to be, well, more Global.