Active not Passive

Trump wants active investments, not passive ones.

Trump has been in the Middle East, raising money for real assets in the US, knowing it will be funded from selling US$ financial assets.

The ‘row back’ on tariffs is consistent with Trump’s negotiating tactics - set a wildly exaggerated target and then row back to your original aim. With around $4trn of imports on an average tariff of 10% and China likely double that, we are looking at around $400-500bn of ‘External Revenue Service’ income.

This is important in the light of this week’s One Big Beautiful Act which includes the act to make Trump’s previous tax cuts permanent. The need to pass this was a key driver behind the early moves to identify cuts in government spending with DOGE. Currently this is stalled by some Republicans for not being tough enough, but is also connected to the announcements on, for example, Drug costs.

This external revenue will also go a long way towards allowing him to take 90% of tax payers out of income tax altogether, something that the markets are not yet thinking about.

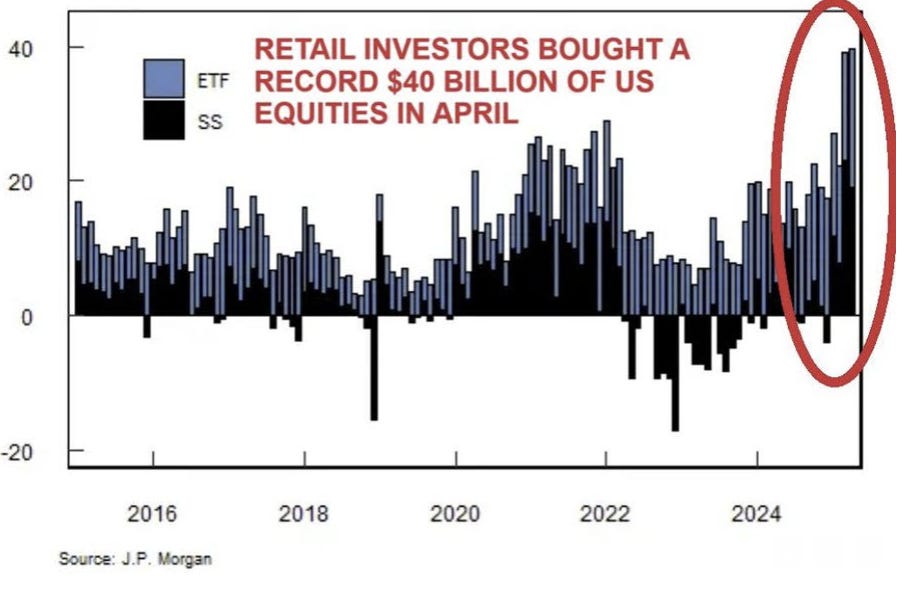

US Retail has ‘bought the dip’, something that has worked for the last five years, but professionals are more hesitant, wary that much of the recent inflow into US equities will start to ‘diversify’ out of US$.

This week, Trump is once again dominating the headlines as he collects tribute in the Middle East, but for us the key message is not about Airforce One’s replacement gift but the message he is giving - and is being received: we don’t want you buying a barbell of US cash and NASDAQ any more, forcing up the $ and giving power to Wall St and billionaires, we want direct investment into Main St. And don’t buy our Treasuries actually, we can just print dollars to do that. Buy Gold.

Trump is basically saying “ We want your US$ earnings recycled into active investments in the US, not passive ones”

The passive flows into US equities in recent years have been enormous - approximately $1.3tn has gone into US Equity Funds since 2020 according to BoA and most of that will have been passive, including a lot from overseas. Indeed, as the FT report this week:

In the five years to June 2024, foreign portfolio holdings of US securities — both equities and all types of debt — rose by $10.3tn, according to the US Treasury. A phenomenal change in share holdings alone made up over $8tn of that.

They go on to point out that 50% of global savings held abroad are currently in US assets and cite a number of strategists all taking about diversification. This is not to say that there is to be the proverbial ‘wall of money’ flowing out of the US, rather that the relatively price insensitive passive investor is not going to be funneling money into the US at the pace that they used to.

Prices are made at the margin and in our view because this flow is not only stalling but starting to reverse, this is the biggest headwind for US Equities.

The key message to us then from the last few weeks has been that a lot of passive investment capital is now embracing the diversification that we have been talking about for some time. First stop, it is going home and we see that as the most likely explanation for currency moves such as the Swiss Franc (see Was it the SWFs? in Fast and Slow Thinking), but also the Taiwanese $ and the Korean Won.

Meanwhile, as we also discussed in the latest Market Thinking Monthly, it looks like US Retail investors ‘bought the dip’ as shown in this JP Morgan Chart (via our friends at Redburn Atlantic).

They also noted that Robinhood’s trading volume was up 26% in April as the pattern recognition from 2020 and 2021 appeared to kick in and ‘it’s all back on’.

And yet, along with many of the ‘professional’ traders, we remain cautious, waiting for the asset allocators to move the big money and in our view that means diversification. US institutional investors are as heavily overweight their own markets as the UK are underweight theirs and while we see scope for rotation, the Mag 7 trade looks ‘exhausted’ in our view. At least from an institutional point of view.

The short term panic over the tariffs may have subsided, but they haven’t gone away. Nor have some of the concerns about AI and the tech bubble

For example, we cited the red flags from Coreweave in our April Market Thinking, concerned how the biggest provider of datacentres for AI training outside of the hyperscalers was heavily indebted, overcommitted and losing money. This week, in its first quarterly report after its (significantly scaled down) IPO it managed to lose $315m on $982m of revenue. Selling $ bills for 70c will always generate lots of sales. Until you run out of $ bills.

It also looks worryingly like 2000-2003 and, as the Yahoo finance chart shows, back then, the market ‘cracked’ in March, then rallied back to the highs by October, before heading south again. But properly this time. The fundamentals that were sending up red flags in March didn’t go away over the summer and we believe that many asset allocation meetings will be looking at this analogue to decide how, not when, to diversify.

Follow the (drug) Money

There have been a number of articles this week talking about how Trump is pivoting because of weak poll numbers, notably with respect to his announcements on Drug Pricing with RFK Jnr, who, now that Musk has stepped back, looks next in line for the Dems/media to feel they have ‘a free hit’ as a way of getting at Trump.

Once again this is a false premise, this was always a plan and part of the need to cut spending in order to be able to pass his bill on tax cuts - something that is being debated in Congress this week - although the main talking points in the US Media appear to be about a book where the Mainstream Media claim that the White House lied to them about Joe Biden’s mental health.

However, while on the one hand we would wish to debunk another Democrat/Media hoax about ‘weak poll numbers’, we would also note that part of Trump’s focus is on the Drug companies precisely because they are one of the main sources of funding for the Mainstream Media - which as we know, has been 92% against him in his first 100 days.

This is about cutting expenditure, but also consistent with his defunding his political enemies via DOGE. Big Pharma funds the MSM.

This chart from Visual Capitalist highlights the issue - and is a snapshot of the top 10 local and national TV spend in June 2023. Obviously Covid meant that for a period everything seemed to be ‘brought to you by Pfizer’. and while they don’t appear in the square for June 2023, they are still a key player.

Meanwhile, according to this site, Pharmaceutical companies spend $6.6bn on advertising, 75% of it on TV ads.

But - and this is important for investors - in the same way that the real target of tariffs is not China but US multinationals, the real target of these reforms are not the Drug companies, but the Pharmacy Benefit Managers, as Mark Cuban (who has done a huge amount of work on this) pointed out in a response to a Charlie Kirk post on X:

Charlie , you aren't close. Drug prices are too damn high. But the big culprit isn't the brand manufacturers, it's the big middlemen. Namely PBMs. They work so hard to distort pricing the first lines in their contracts with everyone is "you can't disclose any of this "

Mark Cuban.

Nothing is quite what it seems, or what we are told it is - especially by the mainstream media who inform a lot of consensus thinking in markets. We see Team Trump as a boardroom full of Gen X business people looking to restructure the US as a business. That means restructuring the balance sheet, cutting head office costs, closing down unprofitable divisions (especially if they are run by hangovers from the previous management regime), sweating existing assets and extracting more of the ‘wallet’ from existing customers. It also means improving competitive position, raising margins and returning value to shareholders (the 90%) rather than the in house managers.

Thus our view on tariffs remains that the real target is US multinationals and their transfer pricing, (sweat assets) but that by setting a 10% base, Team Trump has effectively shifted the tax base from income to expenditure. It may well be that prices rise a little, but the $400-$500bn raised is close to the amount needed to take 90% of US tax payers out of income tax all together. (rewarding shareholders)

Of course it also has the benefits of (some) reshoring and the corralling of many allies into the Blue Team (to improve the competitive position). Interesting to see the latest Foreign Affairs Magazine from the influential Council for Foreign Relations has a long article on how the US is under-estimating China and how it, essentially, needs to assemble a Blue Team. There is, perhaps not surprisingly, more emphasis on the military aspects (and a rehash of the standard rubric about China’s debt and demographics) than we would have, but the point about a giant Customs Union centred on the US is the same as we made last week and while Team Trum probably doesn’t read this substack (!), they do read Foreign Affairs.

(please remember that this is not to be considered investment advice. Please do your own research and speak to your investment advisor).

The wave of faith in U.S. assets is fading, and foreign capital is starting to think about where to go next. At the same time, Trump is saying that they shouldn't leave and should just stay by investing differently

where do you see anywhere that Trump and his administration want to "take 90% of US tax payers out of income tax all together"?

https://paulkrugman.substack.com/p/attack-of-the-sadistic-zombies

By the way, the research about the mainstream media being "92% against him in his first 90 days" mentioned by the The National Desk comes from the Media Research Centre, an American conservative content analysis and media watchdog group - not really unbiased in their analysis

https://www.allsides.com/news-source/media-research-center