Diversification, rotation and the Return of the Cycle.

Market Thinking February 2026

Dictionary.com’s word of the year for 2025 was 6-7, a viral phenomenon among teenagers that seemingly doesn’t mean anything at all.

The reason we have put it in the header of this monthly though is to raise the prospect of the Chinese Yuan being revalued to 6 from 7 against the US$ sometime this year as part of a Grand Bargain between the G2, something not really being thought about at the moment amidst the excitement in the metals markets and the ongoing storm of geopolitical activity.

Were that to be the case, 6-7 would suddenly mean an awful lot for investors.

Bonds and the major Benchmarks have had a sluggish start to the year, while Commodities have ripped and the meme stock brigade have clearly moved into precious metals, which even after the brutal sell off on the last day of the month remain higher, as the return of the cycle awakens commodity markets.

By contrast, Bitcoin and quite a few of the MAG 7 have dropped over 10%, suggesting some powerful rotations are underway and diversification from the US$ is moving mainstream.

Emerging markets have been strong along with most ‘weak $’ plays except oil. New and alternative energy, along with strong narrative plays like Space and rare earths have also done very well year to date.

Team Trump continues to generate considerable policy uncertainty, including a new Fed Chairman, but perhaps the biggest risk in our view is a Mar a Lago accord to mark the $ down against the Rmb, possibly timed around Trump’s April visit to China.

Some diversification from the US$ remains a sound strategy for international investors in our view and such a view on the $ would change liquidity from a trickle into a flood.

As always, please note that none of this should be considered investment advice. Please do your own research and consult your investment advisor

Recency bias means that many people will be focussed on the boom and bust in Gold and, especially, Silver at the very end of the month, but this would be to miss many, more important, signals.

The blizzard of initiatives from the US continued into the New Year, beginning with the abduction of the President of Venezuela, followed almost immediately by the announcement of a plan to ‘purchase Greenland’ that led to one of the most significant Davos meetings in many years with most agreeing with Mark Carney’s observation that things will not go back to how they were.

We looked at some of the Geopolitics in more detail over at the sister substack (This is not Investment advice, Middle Power Play, the Globalists are regrouping) as well as here (The court of King Donald).

Meanwhile, the announcement of the new Fed Chairman is causing uncertainty in fixed income markets, although in our view he is part of a team that are going to have bigger implications for the dollar than anything else. Hence our take on the possibility of 6-7.

Short Term Uncertainties - volatility and (de)Stable coins

The end of the month produced a sharp pullback in Gold and Silver, as a combination of technical signals and dealer hedging (options expiry on the last Friday) led to extreme volatility, although both metals nevertheless closed up significantly on the month. It remains to be seen whether this was a correction to an overbought position in a bull market (we think this is the case for Gold) or the unwind of a technical position within the equivalent of a meme stock (which we think is the case for silver).

Either way, one interesting feature that was largely overlooked amidst all the noise was that Tether (who we know have been one of the big buyers of Gold recently) basically suspended $182m of Stablecoin in Venezuela on January 11th. On that day, Gold was around $4600 and we suspect that a lot of people holding Stablecoin had a quick rethink at that point, which contributed to the melt up.

The Paradox of de-centralised finance is that it currently centralises control.

Tether has previously suspended Stablecoin when suspicious of illegal activity, but when it does this to people and countries who are deemed to be avoiding US sanctions, then it is a weapon of the US State Department and is now being regarded as such.

Stablecoin in general is at the centre of a battle between the competing corners of the Financial sector; Banks want to keep it unable to pay interest in order to keep their quasi monopoly on cash deposits, while Tech Bros and the Fintech sector want the opposite. Meanwhile the big asset managers want to build their own shadow banking sector utilising elements of both. The lobbying is intense.

Meanwhile, the announcement at the end of the month of a new Fed Chairman Kevin Warsh has introduced a new element of uncertainty. Will he be a hawk, as some think, or will he please his new boss and lower rates? The initial reaction was to the hawkish side, which helped the dollar a little and was blamed by some as triggering the precious metals crash, although we think that more of a coincidence. However, like Trump, we need to watch what he does more than what he says.

Warsh is, though, yet another highly connected, very rich, Wall St insider. He works with legendary investor Stan Druckenmiller, as did Treasury Secretary Scott Bessant, and has previously been a Fed governor, importantly during the Great Financial Crisis. His resignation over (too much) quantitative easing has some positioning him as a hawk, but his recent criticisms of Powell suggest he may be more of a Team Trump player. Hence the uncertainty.

Overall, we suspect Warsh is more of a market practitioner than an academic or a bureaucrat like his predecessors, which we would say is a good thing.

In Equities, one of the biggest risks for investors we highlighted last year was that the market cap concentration in the major benchmarks of MAG7 and a single theme, AI, meant that there were significant risks in portfolios that were tracking those benchmarks who were ranked as ‘low risk’. But more important we thought was that there was now increasing stock specific risk emerging among that small group of Mega Caps.

The MAG7 is fracturing, leaving passive investors struggling to keep up with active

This is now starting to show up in performance. Tesla is up 34% in the last six months, while Oracle is down 34%. Google is up 71%, while Microsoft is down 16%. Nvidia, Amazon and Meta are up slightly over the period, while Apple is up 24%, not least because it doesn’t plan to spend billions on AI infrastructure (Oracle just announced $50bn of new debt will be required for its plans.)

Internationally, TSMC is up 34%, while the memory bottleneck story has seen Samsung electronics +118%, SK Hynix 221% and Micron +281%. Stock pickers are having a field day, while low cost trackers are wondering if it might be worth paying a bit more to track a bit less.

Medium Term Risks - The Importance of Currency

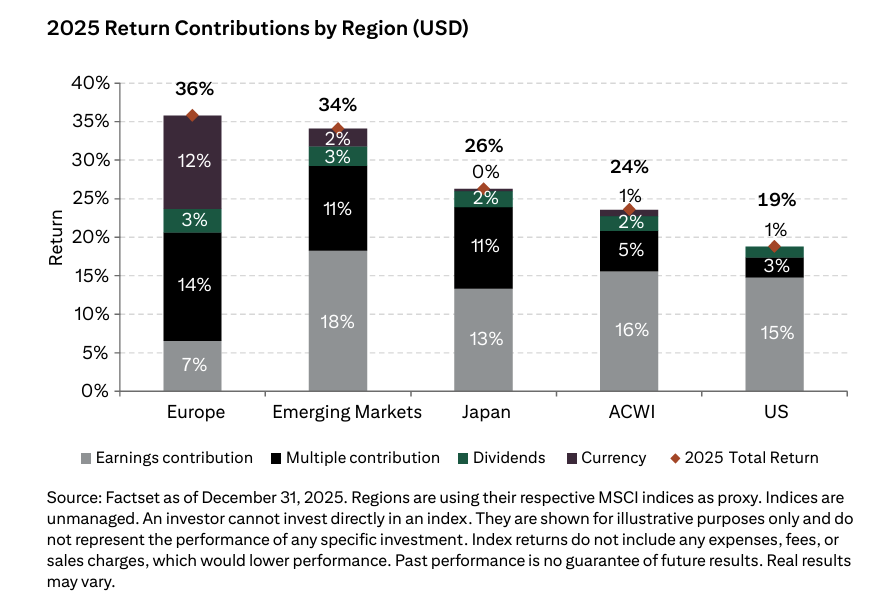

For International Investors - be they US Domestic looking overseas, or simply Global Funds - another major risk is, of course, currencies. The graphic (from Citi) makes several points including this.

Most obviously we can see that of the group, Europe delivered the highest return to a US$ based investor last year, despite having the lowest earnings growth. This partly reflected a bigger multiple expansion than the other markets, but also a 12% return from the currency.

The mechanics of asset allocation are such that a $ based passive or semi passive investor now has to allocate more to the market that has risen in value, which suggests some further capital flows - likely becoming self fulfilling, especially in some emerging markets that have less liquidity.

Trump is moving fast and breaking (a lof of) things.

To say that Trump is moving fast is an understatement. At the beginning of year 1, DOGE and the closing of USAID were about defunding his internal political rivals while this year, in a move that was overshadowed by the noise around Greenland, he has defunded 67 out of 76 international agencies (6-7 again!), mostly associated with the UN, which is, in our view, the real reason that Mark Carney, as spokesman for the Globalists - Trump’s International political rivals - came to Davos with the important speech about the need for Middle Powers to go their own way.

Trump is closing down globalist power structures so they need to rebuild new ones

It remains our view that Trump plans to effectively appoint his successor after the Mid-Terms and will step back but not down. This, we believe, is behind a lot of the recent activities as the rival factions make their play - most notably Rubio and J D Vance (as discussed here).

Greenland has its own strategic dynamics to do with National Security and Mineral rights, but there is also no doubt that, as a Real Estate guy, Trump’s personal ambitions and idea of legacy would love to acquire a vast piece of Real Estate for the US - hence his talk of a ‘purchase’, referencing the Louisiana Land Purchase, or the $7m purchase of Alaska from Russia in 1867 (which was ironically when the British were last fighting Russia and was aimed at reducing their influence).

We discussed the strategic importance of Greeenland at the sister substack here where we also looked at the importance of Space and the future of defence, two investment themes we favout at the moment that we discussed in our previous post (Yin and Yang).

Trump’s Calendar

Which brings us to the Calendar for Trump between now and the Mid Terms. Perched right in the middle of course will be the July 4th Celebrations of the 250th anniversary of the founding of the United States, alongside the Football World Cup (expect the US to try and place second in its group so the team can be playing in Dallas the night of July 4th). Between and then there is much work to do and we would focus on the planned trip to Beijing in April where we suspect that there is a Grand Bargain to be made.

Trump’s trip to Beijing offers another legacy opportunity and we wonder if it will be a Grand bargain that involves a Trump Plaza Accord - i.e a 20% revaluation of the Yuan

China is conscious that its massive export surplus is a problem for other economies and is already showing signs of trying to promote imports. In this it would clearly be helped by an appreciation of the Rmb, perhaps to a target around 6, rather than 7.

Should there be some sort of deal like this then it would obviously benefit emerging markets and exporters generally as well as fuel a greater flow of international capital to China itself.

Possible Plans (what we would suggest…)

In terms of the Calendar, we need to work backwards from the Midterms, which are in exactly nine months from now (November 3rd). With the summer taken up mainly with bread and circuses, we would expect the ground to be laid for a Grand Bargain with China in the ‘first trimester’, to be confirmed in the third.

The third Trimester would then also feature an announcement of a plan to use the proceeds of the tariffs to deliver a large Federal tax cut to the bottom 90%. With $4trn of imports, the target of $600bn is not unrealistic which would be enough to eliminate Federal Income taxes completely for the bottom 90% of voters.

This would set up the Democrats to argue that the tariffs were a bad idea and that taxes can’t be cut. Or agree that tariffs are a good idea.

Long Term Trends - Multi-Polar Capital Markets

Our long term thesis is that the US administration want to maintain the role of the US$ as the world’s trading currency, but no longer want the full burden of being the world’s reserve currency, which links to the points on Stablecoin mentioned above.

Overall this recent behaviour looks to us like a continuation of something we said in a post about Trump last year:

Active versus Passive, May 2025

The surplus countries have certainly be buying Gold, but by paying no interest on Stablecoins means that part of the US policy is making sure that international trade continues to use the US$ for transactions, but not necessarily for savings.

This goes back to the Keynesian notion of the Bancor, something we first discussed in the old market thinking blog and allows the US$ to be central to trade without the burden of necessarily being the Global Reserve Currency.

As stablecoins currently pay no interest they prevent hoarding by surplus countries, but also prevent crowding out of bank deposits. This, however, is a massive source of lobbying and counter lobbying between the Banks and the Crypto Bros.

Equally, an upward sloping yield curve and a shift to US Treasuries being held by US corporates and citizens means that more of the interest bill - which is now hitting $1trn a year - will stay in the US economy.

Currently around $330bn a year of US Government debt interest flows abroad

This is a point we have made in the past about Japan, where over 90% of its $200bn+ of government debt payments remain in the country. When consumers are net savers, as they are in Japan, cutting the return they receive in interest rates does not encourage them to spend and certainly not to borrow and spend. As such, the US centric economic models that assume lower rates stimulate the economy not only fail to work, but actually have the opposite effect.

To this evolving landscape we can add the ongoing development of the Chinese Capital and Savings markets, which, as we discussed in the December Market Thinking (Year Ahead) demonstrated its sheer size and potential with the amount of cash committed just to the Moore Threads IPO - in excess of $4.5trn. Much of this is for ‘stagging’ and speculation, but increasingly this will be sticky and remain in capital markets. Indeed, we think this is part of the strength of the China markets year to date.

Finally, the schism between the US and Europe has clear implications for Europe and the need for its own Capital Markets. As we noted in our discussion on Davos (linked earlier), the Globalists are having to regroup and, likely, will reverse Europe into the existing Global Institutions that Trump is leaving, mostly under the UN ‘Brand’, and that will include the Supra National Financial Institutions like the IMF and BIS, but also the World Bank and the European Investment Bank. Links with the New Development Bank promoted by the BRICS could put the Globalists at the centre of a Global Ex US system.

The EIB meanwhile could be central to a new European Capital Markets system initiative, along with a number of other existing - but largely (as yet) unconnected institutions.

The creation of a European Capital Market would, in our view, be part of a wider range of moves towards ‘independence’ from the US across a range of key industries. Obvious areas include having a home grown version of the MAG7 - i.e a European Google, Amazon and Meta as well as the Robotics and Space aspects of Tesla.

This involves not selling strategic assets to ‘foreign entities’ - and we notice that last week France blocked the sale of Eutelsat’s ground antenna business on Sovereignty grounds.

In our view this will extend to blocking a lot of PE and PC companies coming in for European Assets - although it’s largely too late for the UK as we discussed here in a post from 2024 (Political Cicadas) and is described in detail by Angus Hanton in his 2024 book Vassal State .

The important thing for investors we think is how the favoured status for US multinationals might now change, especially on tax but also on market access and hard won (and lobbied for) monopoly or semi monopoly status.